MiFID II - Cost of Research

Table of Contents

With MiFID II’s implementation date less than three months away, the real cost of research under the new regime is looming large. According to Greenwich Associates research based on interviews with 164 equity traders and 198 equity-focused portfolio managers of European asset managers, hedge funds and insurance companies, the average cost for research/advisory services is 3.9 bps of assets under management.

With the majority expecting that cost to stay flat in the coming year, only 13% of portfolio managers expect their budget for external research/advisory services to increase in the next 12 months, while nearly a quarter of PMs expect their budgets to decrease.

Explicit Payments for Research

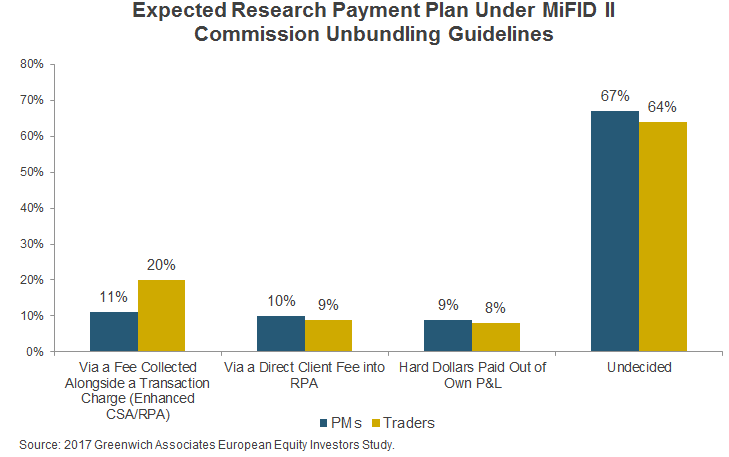

Under MiFID II, investment firms will have to make explicit payments for research, rather than bundling research services in with the commissions paid for trading. In the spring of 2017, 1 in 5 European Tier 1 portfolio managers (who account for over 45% of the total commission wallet) and 43% of buy-side traders told Greenwich Associates that this explicit cost of research would now be passed onto investors via a research payment account (RPA).

In contrast, only 9% of portfolio managers expected to pay hard dollars out of their own P&L (essentially the firm’s money, rather than their clients’ money). At the time of interviews, a majority were still undecided.

With the “big bang” date quickly approaching, however, and as asset managers dig more deeply into the details of the MiFID II unbundling regulations, they have realized that setting up RPAs with every client would add an overly burdensome amount of operational complexity (i.e., figuring out and agreeing on budgets, putting procedures in place to prevent cross-subsidization, etc.).

Paying Out of Own Pocket

As such, many concluded that using an RPA to pass costs along to investors is not worth the headache. Instead, firms such as Schroders, Invesco and Janus Henderson have announced that they will now pay for research directly out of their P&L—using their own money rather than that of their clients—just as regulators intended.

Despite the hit to the bottom line, firms paying out of their P&L will enjoy several benefits: increased transparency of the total costs of investing, reduced operational costs associated with regulatory requirements and a way to differentiate themselves from their non-paying peers that pass on costs to investors. In addition, many of these firms will look to build up their internal research teams to limit the cost of external research, instead investing that money in-house.

Lower Cost of Research

Despite the groans of an industry scrambling to make sense of this new way of doing business, regulators may actually get what they want. As asset managers assess how much research they really need, they should ultimately become more efficient buyers. Further, it is likely that the total cost of research will end up much lower than today’s 3.9 basis points. With active management fees of around 75–100 basis points, the new hard costs for research will represent a hit to margins. For many, this is a price worth paying.