Time for a Fresh Look at the Trade Through Rule

Fundamental change may be coming to U.S. equity markets

December 20, 2016

By:

Richard Johnson

Fundamental change may be coming to US equity markets, and it’s not just because of the new Trump administration. In September, the SEC included Reg NMS in a list of regulations to be examined pursuant to the Regulatory Flexibility Act (RFA). Passed in 1980, the RFA requires government agencies to periodically review and assess the impact of regulation on US businesses.

Regulation NMS is one of the most significant and controversial pieces of equity market regulation, and the aftershocks still reverberate today, over 10 years after it was passed. There were four main components of the regulations:

- The Access Rule – which promoted fair and non-discriminatory access to quotations displayed regulated exchanges through private linkages, and set caps on the fees exchanges could charge.

- The Order Protection Rule – also known as the trade through rule, mandated that investors receive the best price on routed orders by requiring exchanges to route orders to other exchanges if they are displaying better prices.

- Sub-Penny Rule – which prohibited the quotation of prices in increments of less than one penny, unless the stock price is below $1.00.

- Market Data Rules – related to the allocation of market data revenues to SROs/exchanges.

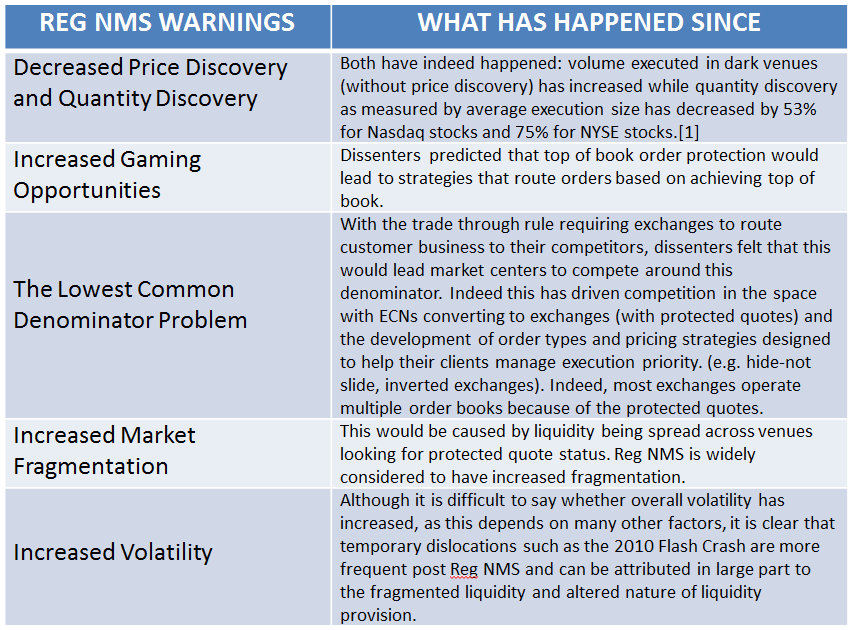

While I am in favor of a holistic review of market structure that encompasses all aspects of U.S. equity market structure, the Order Protection Rule deserves particular attention. This particular rule within Reg NMS was controversial from the beginning and two SEC commissioners voted against Reg NMS at the time focusing on the Trade Through Rule in their dissent. One of the dissenting SEC Commissioners was Paul Atkins who is now a leading figure in President-Elect Trump’s transition team; so it is instructive to look back on his original objections.

While there is clearly correlation between the dissenters’ warnings about Reg NMS and what has transpired, there are many other factors that may have contributed to causation. Nevertheless, the combination of ongoing dissatisfaction with equity market structure, Mr. Atkins’ influence within a new administration looking to scale back financial regulations, and the review initiated via the Regulatory Flexibility Act mean that a fundamental review of equity market structure, including the trade through rule, is increasingly likely.

Reforming The Trade Through Rule

Reform of the trade through could come about by outright abolishing it or implementing an opt out. (At the time reg NMS was being developed some commentators suggested an opt out to the rule for sophisticated investors, however this did not come to pass). In either case it would likely have significant impact on markets. The potential impact could be:

- Defragmentation – With top of book quotes no longer protected by law, exchanges may instead seek to consolidate liquidity on one or two order books. Note: BATS currently operates four order books, NYSE has three and Nasdaq has three, and additionally Nasdaq holds licenses to operate two more equity exchanges.

- Reduction in Complexity – There could well be some reduction in complexity as order types designed specifically for the order protection rule would go away – such as ISOs and price sliding order types. However, exchanges may well devise new order types to reflect the new regulatory regime.

- Shifting Technology Requirements – Much of the technology built to support this rule would become unnecessary. However, brokers will need to upgrade their routing technology to reflect the absence of the trade through rule.

- Increase in locked and crossed market– A locked market is where a bid on one exchange is at the same price as an ask on another exchange. A crossed market is where a bid on one exchange is at a higher price as an ask on another exchange. Under Reg NMS these are effectively banned as the trade through rule should ensure that these locking and crossing orders meet and execute. Without this requirement in place we will likely see an increase in locked and crossed markets. However, these types of situation should self-correct quickly driven by market forces.

It may seem that there are many advantages to reforming or abolishing the trade through rule. It would likely have strong support from electronic market makers who bemoan the complexity it adds to their business operations. Many institutional investors would also support getting rid of it or opting out; with sophisticated smart order routers and algos at their fingertips they may feel they do not require the proscriptive government mandated requirements to tell them how they should source liquidity and achieve best execution.

However the full impact of a repeal of this rule cannot be estimated. To ensure that we avoid mistakes of the past and minimize unintended consequences, a review of the Order Protection Rule should be undertaken in conjunction with a holistic review of equity market structure.

1. http://www.capitalthinkingblog.com/2015/10/sec-equity-market-structure-advisory-committee/