Table of Contents

The adoption of Japan’s Asset Owner Principles could trigger a surge in demand for outsourced chief investment officer services (OCIO) among pension funds and other institutions.

The government of Japan established the Asset Owner Principles in 2024 as part of its broader set of investment, governance and risk management reforms aimed at improving institutional investment outcomes, enhancing long-term investment returns for savers and strengthening the country’s capital markets.

Whereas earlier reforms had been targeted mainly at Japanese companies and investment managers, the Principles are focused on asset owners. Japanese policymakers concluded that weak governance among the country’s asset owners was contributing to what it saw as the country’s suboptimal institutional investment performance. To rectify that situation, the government developed and issued the Principles, a set of guidelines intended to enhance how large institutional investors, such as public and corporate pension funds, insurers, and endowments and foundations, manage assets and oversee investment managers.

The voluntary guidelines codify best practices and expectations for institutions in governance and fiduciary responsibilities, strategic investment strategies and portfolio allocations, asset manager selection, monitoring and fees, and other areas.

Ultimately, the government’s goal in issuing the Principles was to professionalize Japanese asset owners, many of which have been managing billions of dollars in assets with small investment teams, limited expertise and opaque governance structures.

Professionalizing asset owner investment operations

By encouraging asset owners to tighten governance policies and adopt best practices in investments and other areas, the Principles could eventually trigger dramatic changes in institutional investment operations, portfolio allocations and manager rosters—including a potential surge in demand for OCIO services.

Professionalizing investment operations and modernizing portfolios according to the guidelines laid out in the Principles will increase complexity. Many asset owners, especially smaller institutions, will struggle to marshal the expertise and resources required to operate in this new environment.

As just one example, pursuing the Principles’ ultimate goal of enhancing long-term risk-adjusted returns could lead to a shift in portfolio allocations away from fixed income, especially domestic bonds, toward risk assets, especially alternatives and private assets.

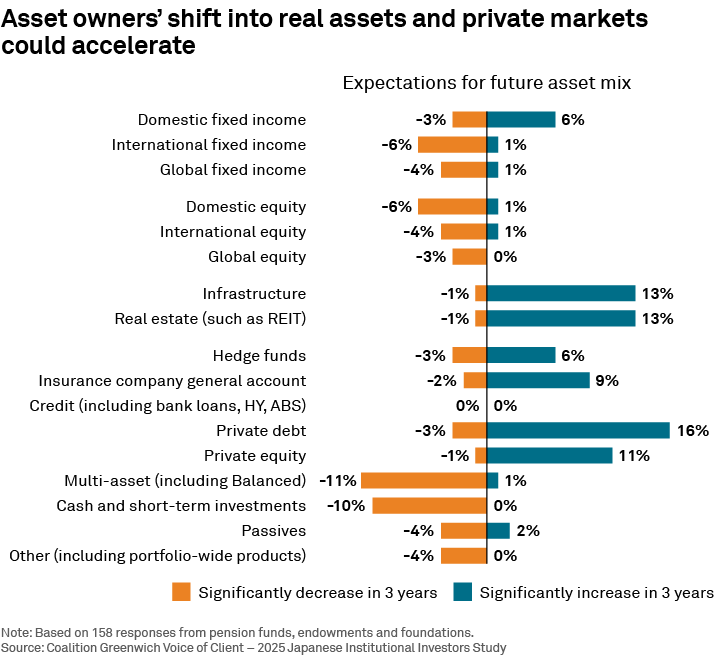

As illustrated in the preceding graphic, Japanese pension funds, endowments and foundations already have plans to expand allocations to real estate and alternatives. Approximately 16% of these asset owners plan to significantly increase allocations to private debt over the next three years, and more than 1 in 10 expect to meaningfully expand allocations to real estate, infrastructure and/or private equity. In each case, only a relative handful of asset owners plan to reduce these allocations.

If the governance and investment guidelines included in the Principles accelerate this move into real estate and alternatives, asset owners will have to contend with the increased complexity that comes from investing in these illiquid and often unfamiliar asset classes. In private debt, private equity, real estate, infrastructure, and other alternative asset classes, investors face unique challenges in cash flow management, valuation, monitoring and risk management, and manager selection/access.

Those tasks would compound new demands arising from implementation of the other governance and investment guidelines spelled out in the Principles. The resulting workloads could strain the operational capacity of some Japanese asset owners, especially smaller institutions.

Some asset owners see OCIO as a potential solution

For some of these institutions, the answer might be OCIO. Currently, only about 3% of Japanese institutions use an OCIO manager. That usage rate is far lower than that found in other institutional markets. For example, over 20% of U.K. institutions use an OCIO manager, as do 16% of U.S. institutions.

If implementing the Principles brought Japan’s usage to levels comparable with these markets, that shift alone would drive huge growth in OCIO. Around the world, most institutions that use OCIO allocate 100% of their assets to the OCIO manager. Factoring in even the smaller group of institutions that use OCIO only for a specific part of their portfolio, OCIO managers claim over 90% of their clients’ portfolio assets on average across North America and Europe.

How likely is it that Japanese institutions will turn to OCIO? One way to answer that question is to look at what services OCIO managers offer and compare that list to projected needs among Japanese asset owners who are in the process of adopting the Principles. The graphic below shows the most common services offered by OCIO managers.

The following graphic shows which of these services resonate most with asset owners around the world. The chart lists the top objectives of asset owners who utilize OCIO managers. Asset owners want OCIO managers to augment their own investment expertise and their access to attractive investment strategies and managers. Asset owners are also looking for OCIO managers to enhance overall investment returns and risk-management capabilities, and to buttress fiduciary oversight and reporting.

Many of those objectives track word-for-word with the guidelines laid out in the Asset Owners Principles. Others reflect some of the likely second-order effects of broad implementation of the Principles. For example, if the enhanced fiduciary responsibility and investment practices introduced by the Principles lead to increased investment in private assets, Japanese asset owners will likely be seeking access to new strategies and managers, some of which might be out of reach for smaller institutions offering smaller mandates. For these asset owners, OCIO managers can provide real value by pooling assets and securing mandates with large, in-demand specialists in private debt, private equity and other asset classes.

A changing landscape for asset management

Adoption of the Asset Owner Principles will have widespread ramifications for the Japanese investment management industry. Changes in the way asset owners interpret fiduciary responsibility, craft and implement investment strategies, choose managers, and allocate portfolio assets could alter the competitive landscape for asset managers. For example, asset owners looking to diversify portfolios might become more open to working with foreign managers and with specialists in private assets, real estate and alternatives.

Increased adoption of OCIO by Japanese asset owners could also have an impact on asset management fees. Declining profitability has been a major challenge for institutional asset managers in Japan, and fee compression has been a big driver of that trend. Widespread use of OCIO by Japanese asset owners could put additional downward pressure on fees.

The entry of OCIO managers would mean more competition for institutional mandates, which could drive down fees. It could also force some managers to discount fees as they are displaced from traditional mandates and instead take on sub-advisory roles for OCIO managers.

To compete in this new environment, both domestic and foreign asset managers will have to make adjustments to their strategies. Those adjustments should include a response to increased demand for OCIO. This process is already underway. In 2025, Nomura announced that it was expanding its OCIO offering in Japan, and existing OCIO offerings from Goldman Sachs Asset Management, BlackRock and other asset managers gained momentum.

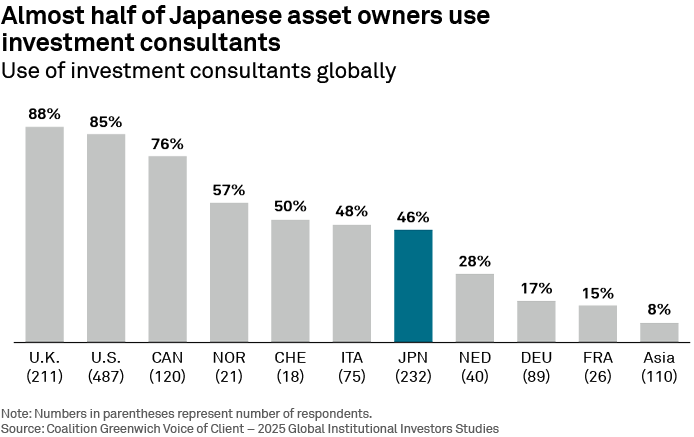

Also in 2025, Mercer announced that it was partnering with Mizuho Financial Group to provide OCIO services in Japan. This announcement was particularly notable in that it brought together the Japanese trust bank industry with the global consulting industry. As shown in the graphic above, about half (46%) of Japanese asset owners use investment consultants, a share that’s up from 43% in 2024. Among Japanese pension funds, endowments and foundations, that share tops 50%.

Meanwhile, trust banks have historically provided Japanese asset owners with many of the services now being offered by OCIO managers, and many Japanese corporate pensions already delegate large portions of portfolio management to trust banks through segregated mandates or advisory structures.

With government reforms pushing asset owners away from traditional approaches and toward more professionalized and formalized OCIO arrangements, it will be interesting to watch the evolution of the market in the coming months and years to see who comes out on top of the OCIO game: trust banks who already have incumbent partnerships with Japanese asset owners, consultants who see OCIO as a way to expand their franchises with high-margin business, or asset managers looking to protect, and hopefully grow, AUM and revenue bases.

Tomomi Shige, Parijat Banerjee, and John Feng advise our investment management clients in Japan.

MethodologyFrom April through October 2025, Crisil Coalition Greenwich conducted interviews with 255 of the largest corporate pension funds, public pension funds, financial institutions, and endowments and foundations in Japan. Total reported fund assets were ¥517 trillion. Senior fund professionals were asked to provide quantitative and qualitative evaluations of their investment managers, qualitative assessments of those managers soliciting their business, and detailed information on important market trends.