Table of Contents

Introduction

North American institutions have been integrating exchange-traded funds (ETFs) into their portfolios for more than a decade. Many institutions in the U.S. and Canada started employing ETFs to execute tactical tasks within their portfolios. As they began experimenting, they viewed ETFs’ liquidity and ability to rapidly access exposures as useful tools in functions like manager transitions, portfolio completion, and liquidity management. As institutions increased their usage of ETFs in these short-term functions, many observed their versatility and began using them across a broader range of applications.

Institutions gradually embraced ETFs as a tool for portfolio management in step with another trend in investing: the rise of passive strategies. As institutions shifted assets from active to passive strategies in large-cap equities and other highly liquid and increasingly commoditized asset classes, they noted that ETFs could work well as a vehicle for taking on long-term strategic exposures. Today, most ETFs in institutional portfolios are passive and categorized as strategic assets, as opposed to tactical.

The ability for institutions to use ETFs as both a tool for tactical portfolio functions and as a means of taking on long-term strategic exposures is leading to increased adoption and expanding allocations. ETF assets under management (AUM) have doubled in institutional portfolios in past years.1 More than a third of institutions have reported plans to increase allocations to ETFs in the next 12 months. Meanwhile, more than half of institutional non-users have indicated they are actively considering introducing ETFs into their portfolios.

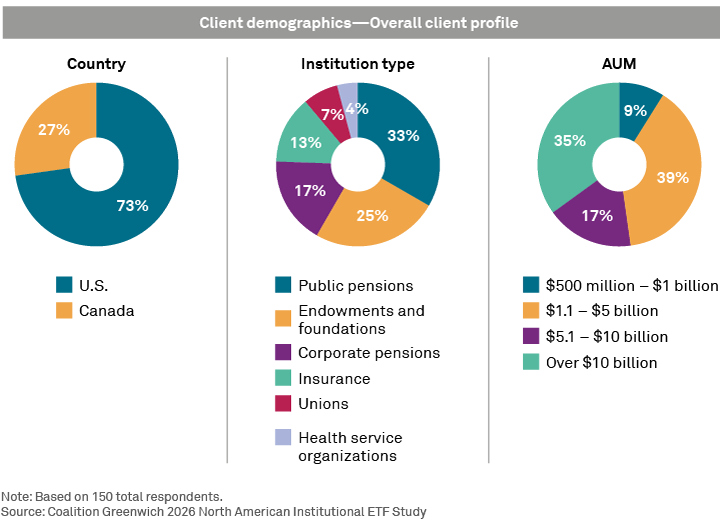

In an effort to learn how institutions are using ETFs, S&P Dow Jones Indices engaged Crisil Coalition Greenwich to interview 150 institutions in the U.S. and Canada. Participants were asked about current allocations and applications, reasons for use, obstacles to ETF investment, expected changes to use and allocation, and other topics. In this report, Crisil Coalition Greenwich draws on the results of that research to present a detailed breakdown of the state of ETF investment in institutional portfolios. S&P Dow Jones Indices has sponsored this report.

ETFs: A growing presence in institutional portfolios

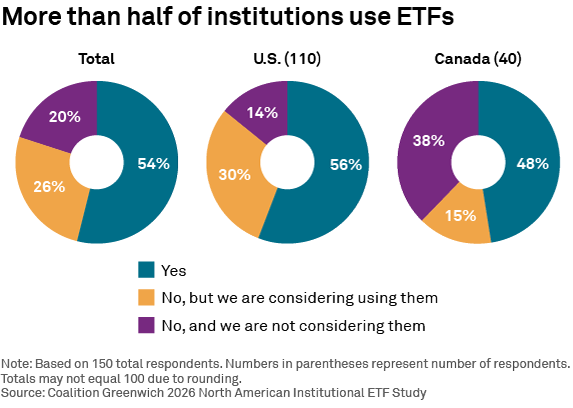

Across North America, more than half (54%) of institutions now employ ETFs in their investment portfolios. Usage rates are highest in the U.S., where 56% of institutions employ ETFs.

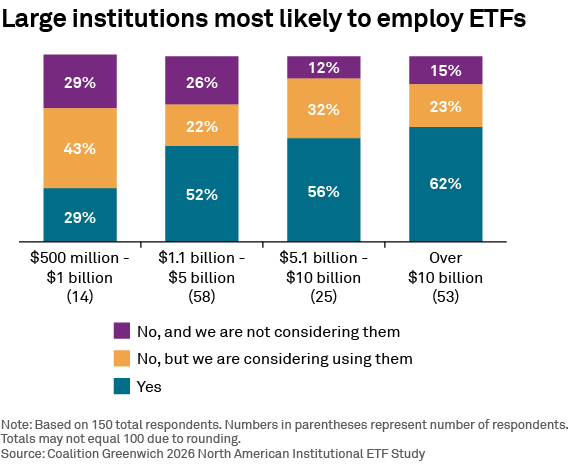

The largest institutions in North America by AUM are the heaviest users of ETFs. Over half of funds with $1 billion - $10 billion AUM and nearly two-thirds of funds with $10 billion+ AUM use ETFs.

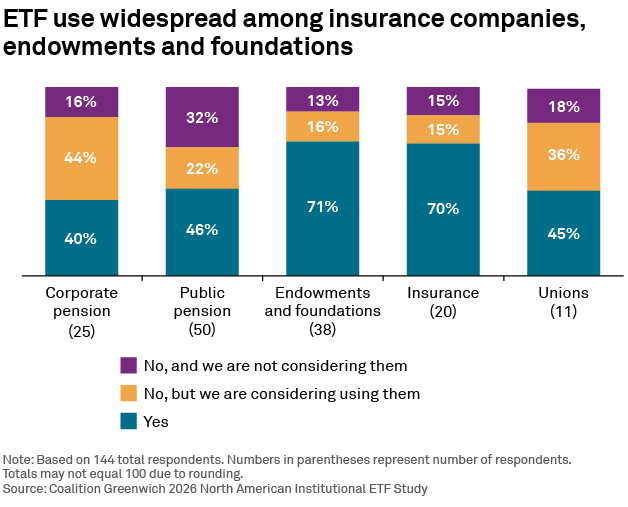

More than 70% of North American insurance companies and endowments and foundations are using ETFs in their investment portfolios. ETF usage is considerably lower among other types of institutions, but as shown in the following graphic, a sizable share of pension and union funds are considering adopting ETFs, including 44% of corporate pensions.

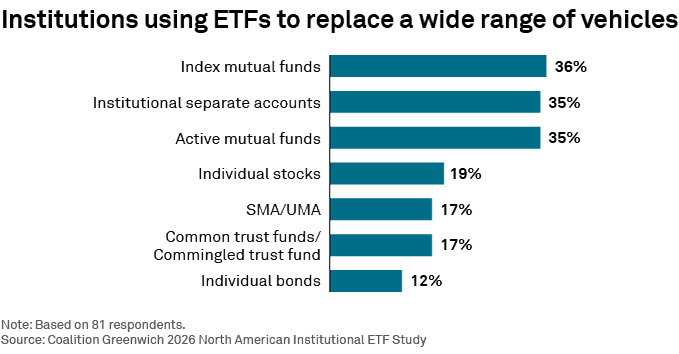

Institutions are using ETFs to replace a wide range of investment vehicles, including index mutual funds, institutional separately managed accounts (SMAs), active mutual funds, and individual stocks (see following graphic). Insurance companies have been by far the most active in replacing other alternatives with ETFs. Meanwhile, 40% of corporate pension funds are using ETFs to replace SMA/UMAs.

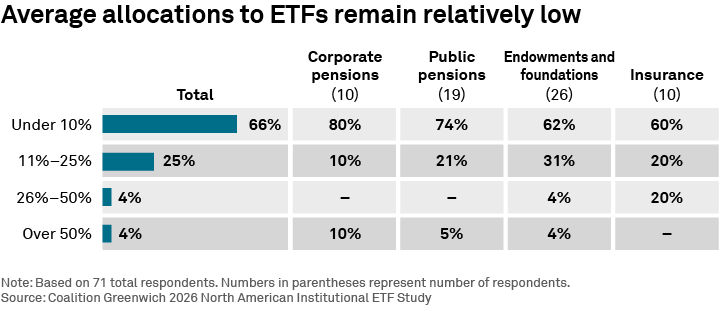

Despite institutions’ broad use of ETFs, actual allocations remain relatively low, with only a third of North American institutions allocating more than 10% of portfolio assets to ETFs. Smaller institutions have built bigger allocations. Among the largest institutions in the study (those with more than $10 billion in AUM), nearly 90% of ETF users allocate less than 10% of total assets to ETFs. Among smaller institutions, nearly half (46%) allocate more than 10%. On average, endowments and foundations, which often face fewer investment policy restrictions than other institutions, report the largest ETF allocations.

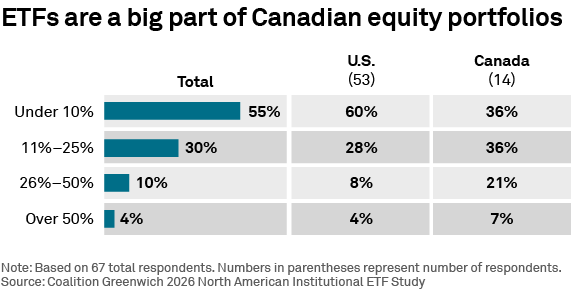

Although overall allocations remain relatively limited, ETFs comprise a growing share of institutional assets in equity portfolios—especially in Canada. Across North America, almost 45% of institutions allocate more than 10% of equity assets to ETFs. Among Canadian institutions, nearly two-thirds are allocating more than 10%, and more than a quarter are allocating more than 25% of equity assets to ETFs.

ETFs have topped 10% of assets in about 41% of institutional fixed income portfolios.

Why are institutions using ETFs?

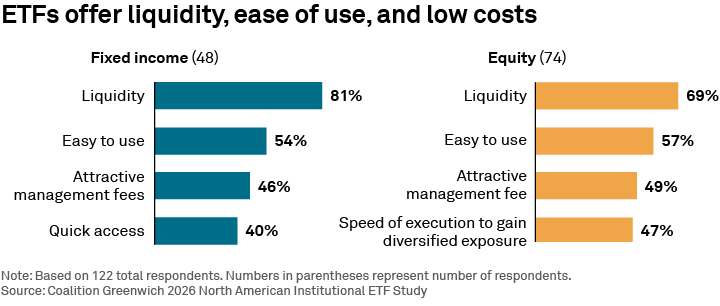

Institutions are adopting ETFs in an effort to access what they view as important benefits. A key consideration is liquidity, which institutions cite as the top reason for using ETFs in both equities and fixed income. Institutions also value their ease of use and ability to provide quick access to exposures across asset classes. Additionally, institutions value ETFs’ low management fees and trading costs.

From a portfolio management perspective, institutions view ETFs as primarily a tool for capturing beta, as opposed to generating alpha.

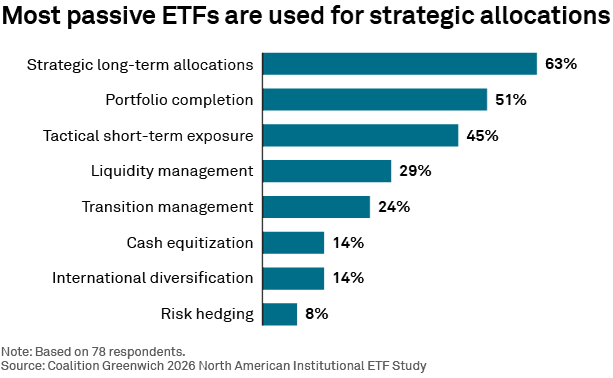

Accordingly, institutions are adopting ETFs as a key vehicle to seek index exposures. Nearly two-thirds (63%) of institutions say they use ETFs in an effort to obtain strategic long-term exposures—usually as part of passive allocations in core-satellite portfolio constructions—making this the most common reason that North American institutions use ETFs. Given that usage, the continued growth of passive strategies in institutional portfolios may help to drive future increases in ETF adoption and allocations.

Passive strategies and strategic exposures

Crisil Coalition Greenwich has been tracking the use of ETFs in the institutional marketplace for more than a decade. From that research, we have learned that most institutions began using ETFs as a tool for executing tactical functions within their portfolios. As they employed ETFs in this manner, institutions discovered that their flexibility, liquidity, and relatively low cost make them versatile tools that are effective for a wide range of functions.

Institutions’ increasing comfort with ETFs dovetailed with their growing appetite for passive strategies. Approximately a third of North American institutions allocate at least a quarter of their assets to indexed investments. That share approaches 40% among public pensions and reaches half of assets for insurance companies. Almost all institutions (98%) are indexing at least some assets.

The growth of indexing in institutional portfolios has been driven mainly by a shift in perspective about the long-term effectiveness of active strategies in highly liquid markets like large-cap U.S. equities. Seeing little opportunity for alpha generation in many increasingly commoditized public markets from their viewpoint, institutions are forgoing active strategies in favor of low-cost passive strategies that are designed to capture market beta and complementing these “core” beta holdings with active “satellite” allocations in asset classes with higher alpha potential.

Traditionally, institutions have used a mix of institutional mandates, separately managed accounts, collective investment trusts, and index mutual funds as their primary vehicles to seek passive exposures and market beta. Today, a growing number of institutions are adopting ETFs for passive exposures, with nearly 90% of institutional ETF users employing passive equity ETFs in their portfolios and 54% using passive ETFs in fixed income.

As more institutions adopt ETFs in an effort to take on index exposures, ETFs have evolved from being mainly a tactical tool to being primarily a vehicle for implementing long-term strategic allocations.

Institutions categorize nearly two-thirds of their current passive ETF holdings as strategic in nature.

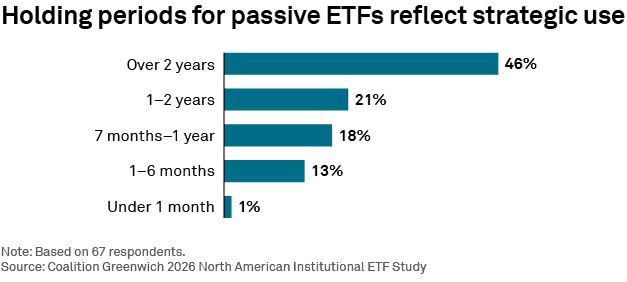

This description of passive ETF use as being mainly strategic in nature is supported by average holding periods. Two-thirds of institutions report average holding periods of a year or more for passive ETFs, with nearly half (46%) reporting an average of more than two years.

Canadian institutions are active users of active ETFs

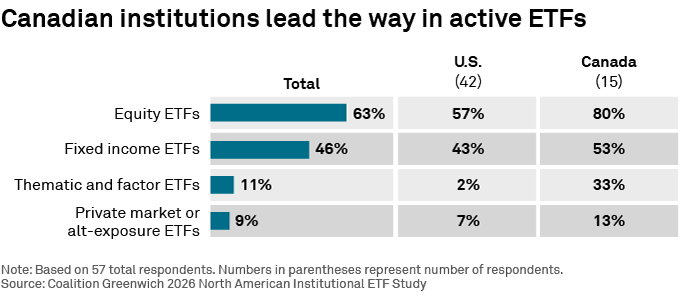

Although institutional ETF holdings frequently use passive strategies, a sizable share of North American institutions invest in active ETFs, especially in Canada. Approximately 80% of Canadian institutions have used active equity ETFs in their portfolios, as opposed to only 57% of U.S. institutions. In fixed income, 53% of Canadian institutions have employed active ETFs, compared to 43% of U.S. institutions. The same trend has been observed for thematic and factor ETFs, which have been used by a third of Canadian institutions versus less than 5% of institutions in the U.S.

Institutional allocations to active ETFs remain minimal. Currently, less than 10% of ETFs in institutional portfolios are active. Across all institutions in the study—including both users and non-users—about 1 in 5 report allocations to active ETFs of greater than 10%. Endowments and foundations were noted as being likely to report no allocations to active ETFs.

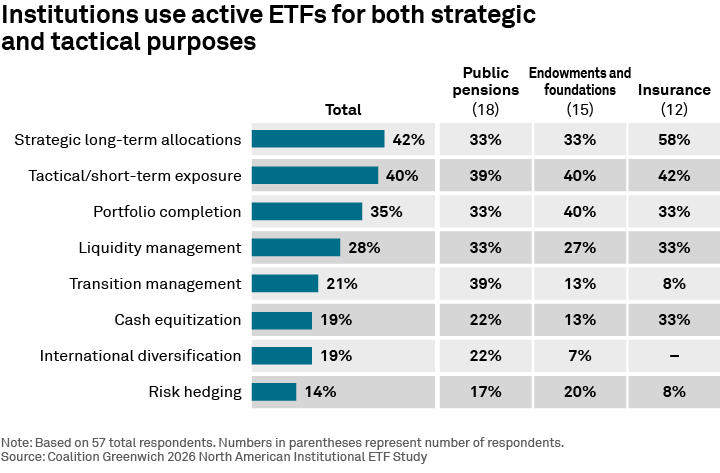

While institutions see passive ETFs primarily as vehicles for long-term strategic exposure, respondents have mixed views on active ETFs. As shown in the chart above, institutions are roughly divided, with about 40% each saying they use active ETFs mainly for strategic allocations or for tactical, short-term exposures. Across North America, insurance companies and institutions in the U.S. are most likely to use active ETFs for long-term strategic exposures, while Canadian institutions are considerably more likely to use the funds for tactical applications. The largest North American institutions—those with more than $10 billion in AUM—are seen as likely to use active ETFs for tactical or short-term exposures.

ETF growth in institutional portfolios

ETFs are common holdings in institutional portfolios. Large North American institutions were frequent early users of ETFs. Today, institutional investors of all sizes are adding ETFs to their portfolios. In terms of adoption, public pensions and insurance funds are catching up to endowments and foundations, the earliest adopters of institutional ETF usage. Given that allocations to ETFs still average below 10% across all types and sizes of institutions, there appears to be potential for growth.

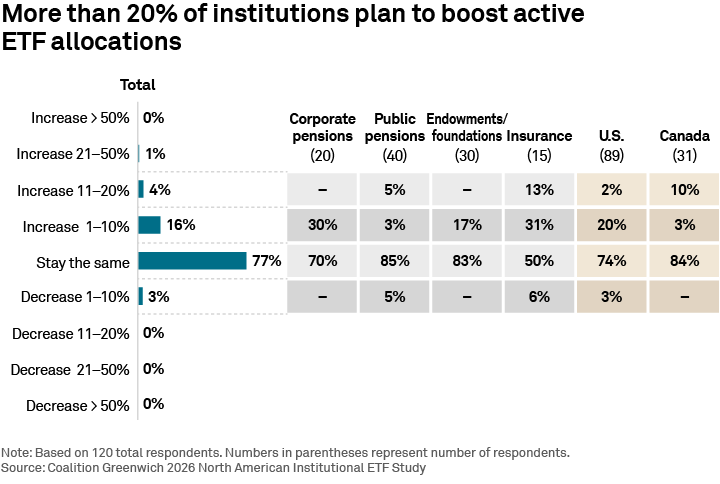

Over 20% of North American institutions are aiming to increase allocations to active ETFs in the next three years (see graphic above). Approximately 30% of corporate pensions and insurance companies seek to expand active ETF allocations.

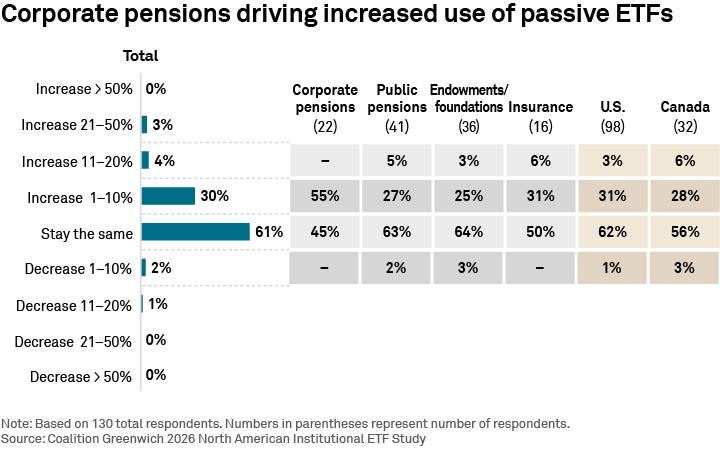

With most institutions using ETFs primarily as a means of taking on passive exposures, institutional use and allocations could get a lift from the continued shift from active to passive strategies. More than 35% of institutions overall and more than half of corporate pension funds aim to increase their use of passive ETFs in the next three years.

As shown earlier in (see chart titled More Than Half of Institutions Use ETFs), more than half of institutions not currently investing in ETFs of any type say they are considering adopting the funds. That group represents roughly a quarter of all institutions across North America, including 30% of U.S. institutions overall and 15% in Canada.

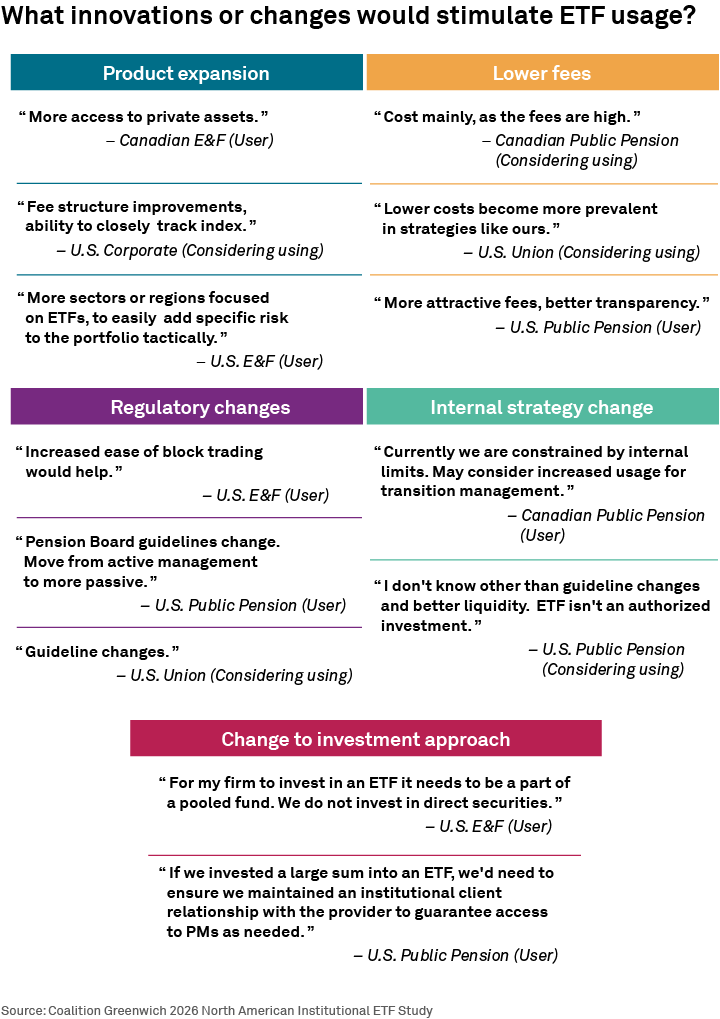

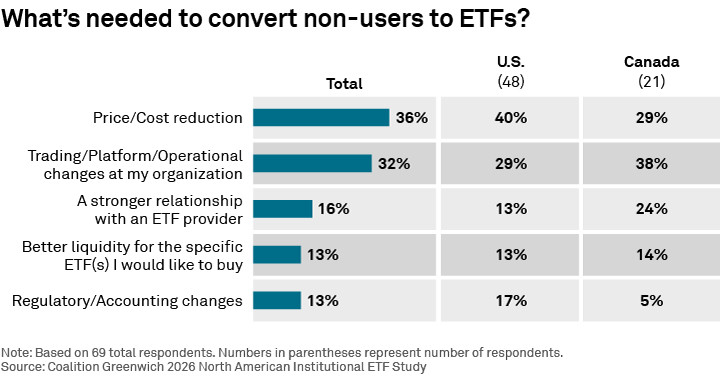

We asked both users and non-users what changes they would need to see to significantly increase their use of ETFs (see graphic that follows). To stimulate usage, institutions want lower fees, product expansion, and changes in regulations, internal strategy, and approach to investments.

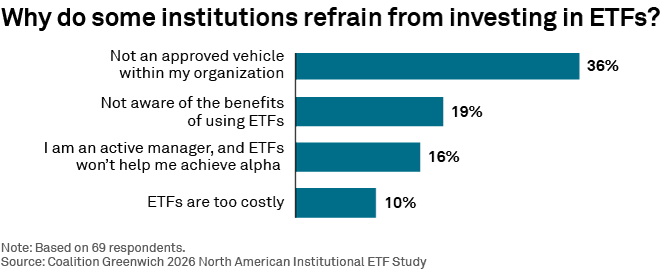

There are some important additional steps that asset managers and the industry can consider. According to the study results, many institutions are also not investing in ETFs because those financial products are not approved vehicles within their organizations. In fact, this is the top reason non-users give for refraining from use. In addition, many non-users are simply not aware of how ETFs can benefit their portfolios and strategies.

Both obstacles can be addressed through better education. Institutions learn about ETFs primarily through various sources including ETF issuers and index providers. Outreach programs by these entities, in collaboration with industry associations and other groups, can educate portfolio managers, analysts, and traders about potential benefits, such as ETF flexibility, liquidity, ease of use, low management fees, quick access to exposures, reduced trading costs, and others. Institutions in the study say the most effective educational resources for conveying this information are detailed product guides and index-level analysis, along with case studies highlighting how other institutions have implemented ETFs.

As investment teams learn about these benefits and watch peers use ETFs, some will begin to advocate internally to add ETFs to their lists of approved vehicles. In some cases, institutions may also have to implement changes to trading platforms and operational systems to allow for the broad use of ETFs.

For institutions in Canada, gaps in internal platforms and operations are obstacles to ETF adoption. U.S. institutions have a slightly different perspective, noting that the one change that would most encourage them to adopt ETFs would be a reduction in ETF costs.

Conclusion

The results of the Coalition Greenwich 2026 North American Institutional ETF Study point to sustained growth for ETFs within institutional portfolios. Continued increases in both usage rates and allocations may be driven in part by the ongoing flow of institutional assets from active to index strategies and the increased use of ETFs as a vehicle for taking on long-term strategic passive exposures.

Meanwhile, the research indicates that institutions of all types and sizes are continually adopting both active and passive ETFs as tools for a variety of tactical and strategic functions. The fact that more than half of current institutional non-users are actively considering introducing ETFs to their portfolios suggests potential for short-term growth. So does the fact that more than a third of North American institutions are planning to increase allocations to ETFs in the next year.

Given those data points, ETF use appears to have entered the mainstream and is now broadly applied across asset classes and portfolio functions by North American institutions.

Susan Gould works with our investment management and investment consultant clients in North America.

113F Filings compiled by S&P Global Market Intelligence.

MethodologyBetween February and April 2026, Crisil Coalition Greenwich conducted a research study to examine how ETFs are used and perceived in the North America institutional investor marketplace. 110 institutional investors in the U.S. and 40 in Canada completed online questionnaires.