Table of Contents

Asian institutions are diversifying portfolios and seeking new sources of yield by shifting assets to more narrowly focused investment strategies.

The four firms named Greenwich Associates 2016 Asian Institutional Investment Management Service Quality Leaders—BlackRock, Goldman Sachs Asset Management, J.P. Morgan Asset Management and Wellington Management—are helping institutions achieve these goals by providing both high-level advice and the specialized investment products needed to implement these strategies.

Diversifying Portfolios

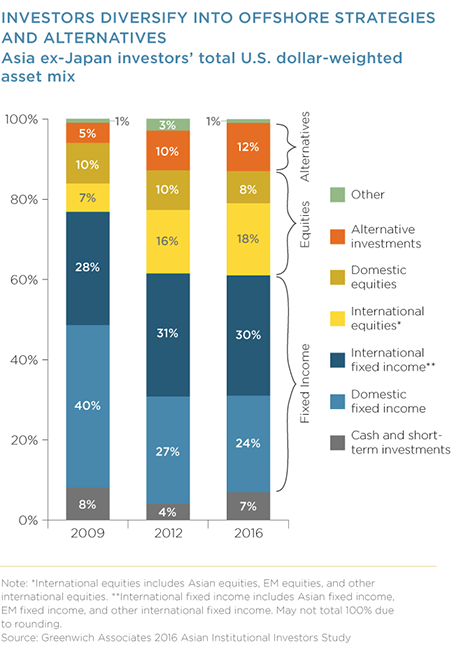

As recently as 2009, Asian institutions had 40% of total assets invested in domestic bonds. Even in relatively large markets like China and India, the limited liquidity available to investors in these bonds meant the allocations that made up the backbone of their investment portfolios represented essentially buy-and-hold investments.

Since that time, institutions have made a concerted effort to reduce their exposures to domestic fixed income and add a more diversified mix of assets to their investment portfolios. Over the period, institutions increased allocations to international equities, which saw the biggest gains, international fixed income, and—in spots—alternatives. Allocations to international equites grew from just 7% of total assets in 2009 to 18% in 2016, with global equity strategies capturing the bulk of those inflows.

Specialized Strategies

More recently, this diversification push has moved into a new phase. Institutions today are moving past global equities and shifting assets into more narrowly focused strategies run by specialist managers viewed as having greater potential to generate yield. They are showing more appetite for credit strategies and for a growing list of approaches ranging from regional strategies to multi-asset and unconstrained mandates.

As they implement these new approaches, institutions in Asia—like those in the rest of the world—are looking for external advice and assistance. Asset managers in the region are now equipping themselves to provide broader support beyond expertise for specific mandates.

Some of these capabilities provide institutions with advice and support on portfolio-wide solutions. Others are more focused and help institutions within the confines of a given asset class or strategy, such as helping the institution define the goals and parameters of an investment mandate.

"There is growing demand for specialist managers as institutions look to strategies with the potential to deliver higher levels of yield, investment alpha and to meet specific risk targets," says Greenwich Associates Managing Director Markus Ohlig.

Alternative Investments

From 2009 to 2012, Asian institutions doubled their allocations to alternative investments. Since that time, aggregate allocations across the region have risen only slightly. However, beneath these flat allocations is growing interest and building demand. Asian institutions have slashed their expected rates of return on every major asset class.

Although Asian institutions remain far more optimistic than their counterparts in Europe and North America, expectations for portfolio-wide returns have been cut to 5% in 2016 from 7% in 2013. Given these reductions, institutions are looking more closely than ever at alternative assets classes such as infrastructure and private equity—the latter of which institutions expect to deliver double-digit annual returns over the next five years.

Currently, most assets invested in alternatives in Asia come from 20–30 sovereign funds and other large institutions that account for the vast bulk of the regions’ institutional assets. Many of these are big enough and have sufficient resources to handle alternative investments such as real estate internally. Often, they supplement their internal capabilities by working with specialist alternative managers such as KKR or Blackstone.

However, as investors across the region seek out new sources of return and diversification, these investors will be joined by as many as 30–40 other institutions that are still large in terms of absolute assets, but are too small to take on the task of running alternative asset classes internally.

This will create a significant opportunity for managers in private equity, infrastructure, commodities, real estate, and hedge funds. Hedge funds are particularly promising for managers, given that most of even the largest Asian sovereign wealth funds have little desire to run in-house hedge fund strategies.

In all likelihood, it will take three to five years for demand from this expanded group of Asian institutions to materialize. Many institutions still lack familiarity and deep understanding of the strategies. Also, many Asian institutions still need to update investment guidelines to allow allocations to alternatives.

"Smart alternative managers have already kicked off marketing and sales strategies aimed at educating these institutions about how they should be approaching alternatives and the role these asset classes can play in an institutional portfolio," says Greenwich Associates consultant Jivan Sidhu.

Growth Opportunity for Managers: Asian Insurers

Insurance companies represent an enticing growth prospect for managers in both traditional and alternative asset classes. The reason: As they diversify portfolios away from domestic fixed income, Asian insurers are allocating growing amounts of assets to external managers.

Domestic fixed income still accounts for 47% of assets in Asian insurers’ portfolios. Overall fixed-income allocations can reach 70%. Like other institutions in Asia, insurance companies are looking for better sources of yield in a low-interest rate environment and more portfolio diversification. Because most Asian insurers’ capabilities are limited largely to their home markets, growing numbers of these companies are turning to external managers.

Although the bulk of insurance assets are still managed internally, external allocations have been growing and now make up some $138 billion. Some insurers in South Korea and Taiwan are now allocating up to a quarter of assets to external managers.

"The recent decision by China Life Insurance Company to start using external managers represents a huge potential source of assets and likely signals the start of a broader trend among insurance companies in China and India," says Markus Ohlig.

Managing Director Markus Ohlig and consultant Jivan Sidhu adviseon the investment management market in Asia.

MethodologyBetween January and March 2016, Greenwich Associates conducted 139 interviews with the largest institutional investors in Asia.

Senior fund professionals were asked to provide detailed information on their investment strategies, quantitative and qualitative evaluations of their investment managers, and qualitative assessments of those managers soliciting their business.

Countries and regions where interviews were conducted include Brunei, China, Hong Kong/Macau, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.