Changes in U.S. Corporate Bond Market: Evolution, not Revolution

I spent most of my summer digging through our 2014 North American fixed income data looking to see what's changed in the past year and what's the come. While the bulge bracket continues to dominate rates, mid-tier brokers are making some headway in credit helped by increased client adoption of electronic trading platforms. But as with most things market structure its never that simple. Despite client demand for high quality secondary market liquidity, the primary continues to dominate. Want an allocation of Twitter's new bond offering? Only the biggest corporate bond players will be able to help you, and then only if they make enough money from you in secondary market trading.

In addition to an analysis of the above client/dealer interaction, our new research looks at the top corporate bond dealers by market share and emerging dealers to watch. We also look at corporate bond trading platform adoption and provided a detailed breakdown of electronic trading by order type and client segment. As the title of the post implies, the corporate bond market is finally starting to show signs of change but we've yet to see the big bang change that many have been expecting. The press release:

CHANGES IN U.S. CORPORATE BOND MARKET: EVOLUTION, NOT REVOLUTION

Investors Increase Use of Electronic Trading and Emerging Dealers, Access to New Issue Allocation Remains Major Roadblock to Change

Monday, September 15, 2014 Stamford, CT USA — The corporate bond market is going through an evolution, but not yet a revolution.

That’s the conclusion of a new report from Greenwich Associates, “Changes in U.S. Corporate Bond Market: Evolution, Not Revolution,” which presents the results of the Firm’s annual North American fixed-income research based on interviews with more than 1,000 U.S. institutional investors.

Investors Open to New Ways of Executing Trades

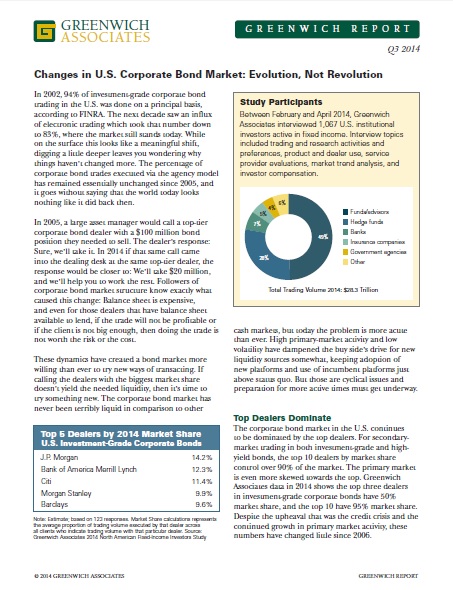

This new report finds that institutional investors are taking tentative steps to utilize new sources of liquidity to execute corporate bond trades and are forming new trading relationships beyond the top dealers—many facilitated through electronic trading platforms. The average number of dealers used is up 35% since 2009. Nevertheless, the corporate bond market in the U.S. continues to be dominated by the top dealers. For secondary market trading in both investment-grade and high-yield bonds, the top 10 dealers by market share control of over 90% of the market.

Competition on the sell side is picking up in large part due to the cost of capital, which is hitting the largest banks the hardest. But while some second and third-tier banks are expected to increase their share of trading in the secondary market, the importance of new-issue allocations to institutional investors will keep the majority of flow going through the largest banks that control the majority of bond underwriting.

Electronic Trading – Size Matters

Access to clients via electronic trading platforms is increasingly providing a boost to dealers hoping to break into the top 10. Greenwich Associates estimates that 16% of institutional investment-grade corporate bond trading volume is executed electronically today, with four out of five institutional investors utilizing electronic trading platforms for some portion of their trading.

“Everyone willing and able to quote a competitive price in response to an RFQ has the ability to win business from the 80% of buy-side firms actively trading corporate bonds electronically—something not possible only five years ago,” says Kevin McPartland, Head of Research for Market Structure and Technology at Greenwich Associates.

MarketAxess continues to be the market share leader in North America, executing 86% of dealer-to-client investment-grade corporate bond electronic trades. Greenwich Associates believes electronic trading of trades between $100 thousand and $5 million in size will continue to grow in the coming years, with the potential to take the market-wide percentage of volume traded electronically to 20% by 2016.

Growth in electronic trading of block trades – those over $5 million – will be a much more challenging endeavor, as these trades are the ones that the buy side brings to dealers via phone, not only for market color and liquidity, but also to build up a relationship that ensures access to sought-after new issue allocations.