Outsourced Chief Investment Officer – Strategies for Sales Success

Table of Contents

Outsourced chief investment officer (OCIO) goes by a number of different names, including “discretionary,” “fiduciary,” and “delegated.” But interest in the topic, whatever you choose to call it, is practically universal. As a result, managers frequently ask us to help them make sense of this increasingly popular scheme and to assess the opportunities (and threats) it presents.

Clearly, by tapping into OCIO intermediaries, managers gain access to otherwise inaccessible down-market funds, open the door to large, more consolidated asset flows, and deepen existing relationships with investment consultants. However, managers are also very aware of the potential downsides, including further fee compression, coverage complexity and disintermediation from the end client.

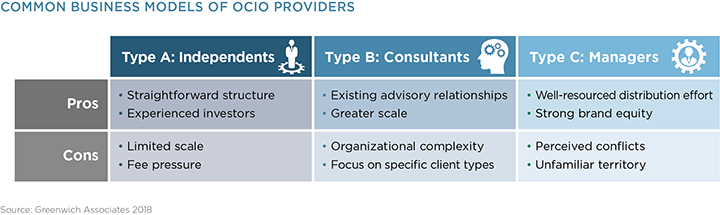

To explore the possibilities of asset managers selling into OCIO providers, Greenwich Associates recently published a white paper, Winning in the New World of Outsourced OCIO, advocating a number of strategies worth consideration. As success in this area requires a nuanced understanding of the competitive landscape, we outlined three popular OCIO provider models and corresponding distribution strategies for each.

OCIO Provider Model Type A: Independent

These are the dedicated, OCIO-only platforms that pair traditional plan sponsor structures with expanded expertise, access and resources. Managers exploring partnerships in this area should focus on the manager research function, ensuring that the firm’s strategies are properly understood and top-of-mind. Additionally, OCIO salespeople should socialize some of the firm’s best thinking with the provider’s leadership to curry greater favor.

As for drawbacks, Independents are often not hampered by existing product relationships or most-favored-nation pricing arrangements (as Type B operators may be). Therefore, managers should be aware of Independents’ pricing power and avoid unprofitable placements, however tempting the large flows may be.

OCIO Provider Model Type B: Consultants

Engaging with consultants who operate in both advisory and discretionary capacities can make for complicated relationship management. But they also offer managers the possibility to leverage existing advisory engagements into discretionary ones. As with traditional investment consulting, the OCIO conversation starts with manager research, as it is often a shared resource, no matter the level of discretion required. Depending on the consultant’s approach to OCIO, managers should then expand the conversation to include field consultants and other OCIO decision-makers.

Note, however, that there is no one-size-fits-all when it comes to investment consultant OCIO structures. Because consultants frame their OCIO offerings differently, managers need to understand the individual consultant’s approach and overarching philosophy to OCIO. This is important, both to engage most effectively with discretionary leaders and to avoid friendly fire with colleagues engaging on the traditional side. Advisory or discretionary, it is the job of the investment consultant to screen out managers who deviate from core investment messages. As such, sophisticated account planning and coordination with mainstream consultant relations is needed to ensure that all communications are crisp and internally consistent across channels.

OCIO Provider Model Type C: Managers

Although managers may cringe at the thought of partnering with their competitors, several of the largest managers now offer open architecture OCIO platforms of their own, so it’s becoming more commonplace. Interests are, in fact, quite well aligned in this arrangement, as the open architecture structure may actually position third-party managers more prominently as a means to stave off the inevitable perceived conflicts of interest.

The difficulty, however, becomes clearer in the sales process. Manager research should still be the starting point, but this is often a small, unfamiliar point of sale. Moreover, broader socialization of the selling manager’s offering needs to be conducted carefully, as the targets of this outreach could be the relationship management and sales people who, on any other day, would act in direct competition.

Know Your Customer

With the numerous shapes and sizes of OCIO distribution channels, it’s no wonder that managers looking to sell into these providers struggle to nail down a comprehensive strategy. Clearly, given all the shades of gray in the space, the distribution strategies that value the flexibility to cater to provider idiosyncrasies over those that approach all channels in a similar fashion will be the most successful.