The return of volatility? It depends on where you look.

We might be getting a little bit closer to understanding whether or not the changes in the capital markets are cyclical or structural. We view volatility - or the lack thereof - as a major factor impacting profitability across financial services. More volatility generally leads to more volume which benefits every market participant who charges on a per trade basis: brokers, dealers, exchanges, SEFs, etc. Even for investors, outside of long-only funds many strategies tend to perform (whether outperform or underperform) when the markets really get moving.

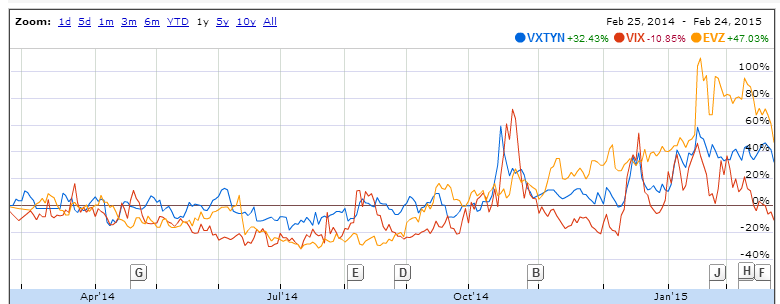

Going under that assumption, equity markets still are struggling to generate any excitement with volatility remaining at historical lows as measured by the VIX, which is down roughly 10% over the past 12 months. But FX and the interest rate markets are showing a different story. As measured by CBOE indices tracing 10 year UST prices (VXTYN) and Euro FX Volatility (EVZ) things are starting to get interesting. The former is up 30% over the past 12 months and the latter up an eye opening 47%.

Why?

The expectation for a rate increase from the US Fed this calendar year at high level explains increased activity in the rates market. As for FX, the Swiss National Bank added fuel to the fire, but the resurgence of what seems to be a bona fide currency war is driving activity from corporate treasures and asset managers alike.

These indices are of course do not track the entirety of the markets they focus on, but for lack of a better proxy they provide interest insight into the direction the world is headed.

Charts are worth a thousand words, so take a look for yourself.

(Source: Google Finance)