Table of Contents

Commercial banks are entering 2026 with a sense of cautious optimism. Although the bullishness that greeted the new year in 2025 has faded, so have the worst fears of the past 12 months, when at times, it seemed like some combination of tariffs, inflation, global conflict, and financial market volatility could push the economy into crisis.

As the new year unfolds, commercial banks are guarding against persistent risks in what remains an uncertain economic environment and working to control expenses in an era of growing technology costs and fierce competition. With expectations for net-interest income expansion in the low single digits, commercial banks will also be looking to leverage loan growth and increased fee income to help drive revenue.

In this paper, we’ll look at the landscape banks will face in 2026 as they pursue revenue expansion through two main channels: inorganic growth in an increasingly favorable environment for mergers and acquisitions (M&A), and organic growth strategies aimed at increasing share of wallet and spend from their existing small business and middle-market clients.

Inorganic growth

A multitude of banks are expressing openness to strategic transactions in the coming year, with many considering both acquisition and sale opportunities. This reflects a broader trend of banks actively evaluating their current position and growth strategies in a rapidly evolving environment. The current climate suggests an increased willingness among banks to pursue M&A as part of their efforts to strengthen competitiveness and adapt to industry changes.

This current wave of bank M&A is being driven by several factors. Banks need to scale effectively to support and manage rising technology costs while remaining competitive. The regulatory environment is generally viewed as more supportive of consolidation, which is providing additional momentum for merger activity. And, as always, banks are pursuing growth opportunities—acquiring deposits, expanding and diversifying revenue streams, and building the scale needed to compete at both a national and global level.

Many banks view M&A in 2026 as an attractive opportunity to broaden their footprint and enhance their offering. However, commercial banks’ clients often view M&A through a different, more skeptical lens. Crisil Coalition Greenwich research demonstrates that bank mergers and acquisitions have often led to significant challenges in client experience, emphasizing the importance of careful evaluation and the need for proactive communication during periods of change.

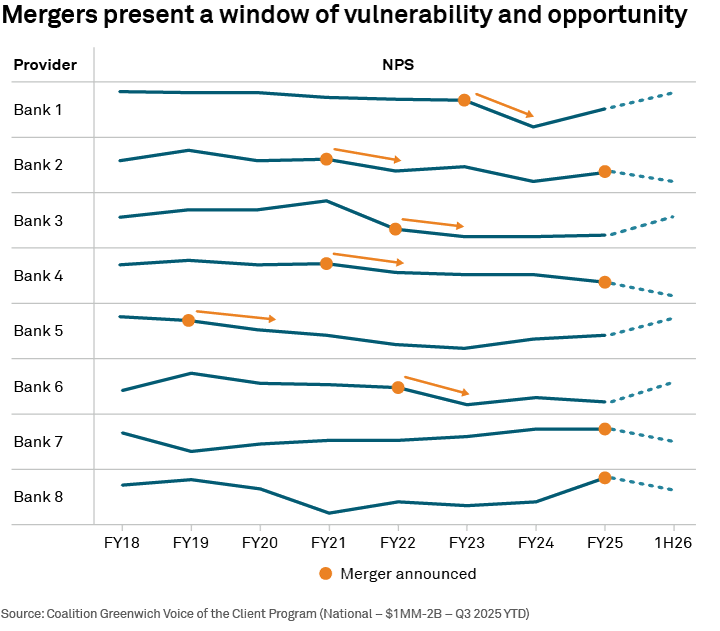

The graphic below tracks Net Promotor Scores for several U.S. banks that have been involved in a merger or acquisition since 2018. NPS, a key indicator of customer loyalty, measures how likely a customer is to recommend the provider. As the chart shows, each M&A transaction was followed by a sharp decline in NPS. On average, banks undergoing an M&A deal experience a 15–20 point drop in NPS, typically lasting between 12 and 24 months.

These findings indicate that the impact of M&A activity on growth is more complex than it might appear on the surface. Although the acquiring bank increases in size and scope, the integration process can be highly disruptive for clients. This disruption often leads to declining client satisfaction and loyalty, creating opportunities for competitors to attract and retain unhappy customers.

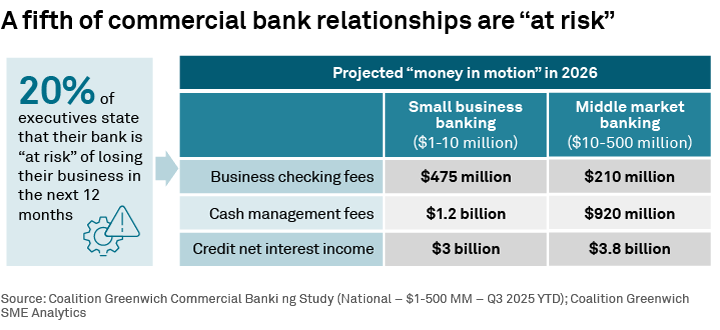

Clients frustrated with a decline in service quality during a bank integration are prime targets from competitors. As M&A activity increases, the pool of these “at risk” clients will continue to grow. In fact, as shown in the preceding graphic, about 1 in 5 corporate executives say their current bank is at risk of losing their business in the next year. Based on average account size, that means substantial revenue could be up for grabs in 2026.

With such significant revenue at stake, it’s clear that bank M&A will be a major driver of bank growth in 2026, both for banks engaging in M&A transactions and those looking to capitalize on client turnover.

Organic and client acquisition growth

Commercial banks can achieve organic growth through two sources: by attracting new clients and deepening relationships with existing ones.

Growth from new clients

As mentioned earlier, due to M&A activity and rising expectations, 2026 presents a unique opportunity for commercial banks to win new clients, particularly those businesses that may be dissatisfied with their current provider. But how should banks approach this?

To effectively engage with these dissatisfied clients and other prospects, banks should focus on two main channels: corporate branding and the sales and marketing process.

Business owners and executives often form opinions about banks well before any direct outreach or communications occur. These perceptions heavily influence their receptibility to solicitations, which is why banks invest heavily in branding every year.

To position themselves for success in winning new commercial clients, banks should carefully consider the messages they communicate. The following graphic highlights the key themes that currently resonate most with prospective clients.

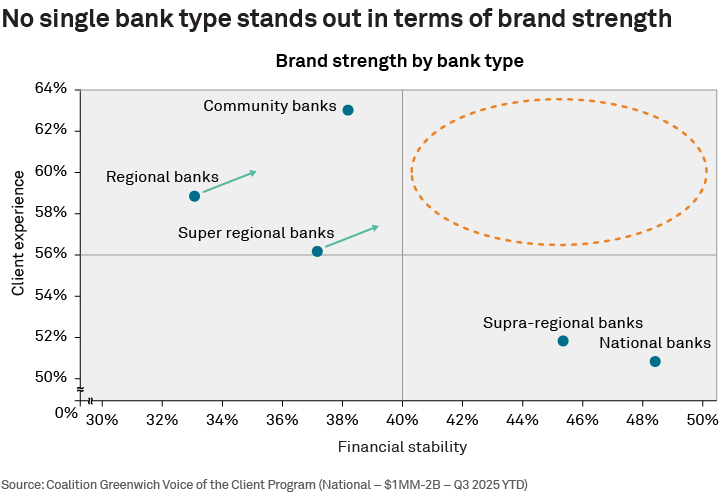

Although the 2023 banking crisis might seem like distant history to the general public, it remains top of mind for many business owners and executives. For these professionals, the series of bank failures and the risks created still loom large. According to Crisil Coalition Greenwich Voice of Client data, financial stability stands out as the most important attribute of a bank’s brand, with client experience and relationship manager (RM) quality ranking as secondary considerations.

Given those findings, an effective brand strategy for banks is clear: Prioritize messaging around financial strength and reinforce a commitment to delivering exceptional client experience. Banks looking to best position themselves to win new business should brand themselves first and foremost as financially stable and, second, as best-in-class for client experience. While this approach may sound straightforward, consistently communicating and demonstrating these qualities require thoughtful execution and ongoing investment.

As shown above, that branding “sweet spot”—combining financial strength with exceptional client experience—remains largely unclaimed in the market. While the biggest national and supra-regional bank brands are associated with financial strength, and smaller regionals and community bank brands are closely tied to top-quality client experiences, no group has claimed both attributes in their brand identity.

For now, each side of the industry is playing to its strengths, with the biggest national and regional banks emphasizing their financial stability and smaller competitors looking to leverage their reputations for great client experience and high-touch service. Any banks that manage to bridge this gap and build brands that embody both financial stability and client experience will give their sales teams a distinct advantage to win new business in 2026.

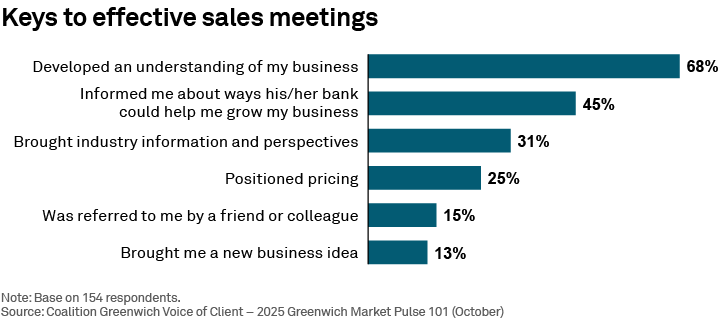

This represents a significant opportunity, especially when most business owners and executives report widespread dissatisfaction with current bank sales efforts—nearly three-quarters consider these efforts ineffective. Strengthening brand messaging around both financial strength and client experience could be a game-changer for RMs and sales teams.

The graphic above highlights areas banks should focus on to improve sales effectiveness and reflects the priorities business owners and executives identify as most influential during sales interactions. The most effective sales calls are those where a banker demonstrates a deep understanding of the clients’ and prospects’ businesses and provides actionable insights and ideas that support growth and efficiency.

To consistently deliver on this level, banks must continue to strengthen their data and analytic capabilities, elevate the quality of advice delivered by RMs, and invest in the technology infrastructure needed to integrate these elements to ensure your bank makes a lasting impression with prospects.

Growth from existing clients

One of the most effective ways for banks to increase wallet share is making it easier for clients to do business with them.

While this may sound simple, delivering a seamless, easy client experience has long been a significant challenge for commercial banks. Part of that struggle comes from the nature of commercial banking relationships. In a highly regulated industry, virtually any action a bank client wants to take requires significant amounts of documentation and review.

Know Your Customer (KYC) and Anti-Money Laundering (AML) rules have made that problem even worse. However, banks also bear some responsibility. Many institutions continue to operate on outdated, legacy technology platforms that make it difficult or even impossible to effectively manage data. As a result, clients are forced to enter the same information repeatedly across multiple forms and to endure long delays. Banks aiming to drive growth by increasing wallet share from existing clients in 2026 must address the ease-of-doing-business challenge.

The first step is clear: Banks need to elevate RM performance and ensure all clients are getting fast and effective responses to their inquiries. Unfortunately, industry trends indicate the opposite—clients across the U.S. report a marked decline in RM performance since 2020, citing notably lower scores for timely follow-up, frequency of visits and the quality of understanding and advice. Reversing that trend will be essential for unlocking internal revenue growth in the year ahead.

In addition, commercial banking executives need to explore revenue opportunities from products outside their commercial product set. Programs that offer benefits to clients’ employees to incent them to bring their consumer business and wealth management products for executives are examples. Developing industry verticals that allow RMs to become experts in high-revenue industries is another tool to deepen relationships.

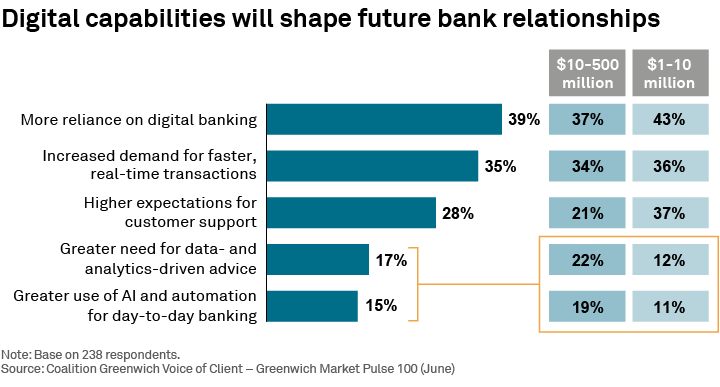

The second step is more complicated, but most banks are already hard at work on a solution. To meet client expectations, banks must offer electronic banking options that simplify day-to-day banking and make life easier for clients. As shown above, digital capabilities will become more important to clients and, presumably, more important drivers of wallet share in the years ahead.

Strategic partnerships

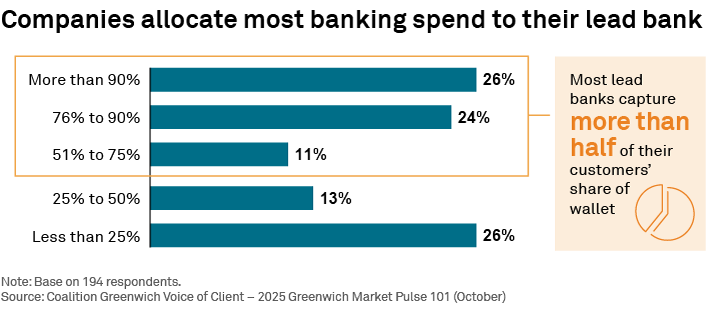

Commercial banks investing in their service propositions and the client experience should have one overriding strategic goal: to become lead provider to their clients. As illustrated in the previous graphic, most commercial banking clients allocate more than half their wallet to their lead providers, and half of lead banks capture more than 75% of the client’s wallet. Achieving the position as lead provider is by far the number one way for commercial banks to expand share of wallet and revenues, and should be the ultimate objective of any bank looking to stimulate organic growth in 2026.

Conclusion

The Greenwich Optimism Index, which gauges the economic outlook of commercial business owners and executives, is hovering close to neutral. After rising into positive territory at the start of 2025 and plunging into the negative in the wake of concerns over inflation and tariff policies, the Index has leveled off at the start of 2026 with a reading just above zero—reflecting a climate of uncertainty. This suggests U.S. small businesses and middle-market companies are on guard against risk, but open to new opportunities.

Commercial banks are responding in kind, entering the new year with plans for a continued focus on risk management and cost controls, while also seeking avenues for growth. In a favorable environment for M&A, opportunities for inorganic expansion are set to play a significant role in bank growth strategies in the year ahead. A surge in M&A could also create new opportunities for banks able to capitalize on disruptions caused by M&A integration to capture new clients and assets to stimulate organic growth.

Cheri Derrick, Chris McDonnell, Don Raftery, and Kevin Seiler advise our commercial banking clients in the United States.