Table of Contents

It’s getting easier for companies to onboard new banks, and corporates in Asia are taking full advantage of this trend as they adjust supply chains and businesses in response to U.S. tariffs.

Tariffs imposed by the Trump administration in the United States are driving a redistribution of trade volumes within existing global corridors. As Asian companies shift their focus from exports to the west to intra-Asian trade and other opportunities, they need cash management providers in new markets.

At the same time, technological innovation has made it easier for companies to onboard new banks, reducing the disruptions and switching costs that have traditionally made companies think twice before bringing on new cash management providers.

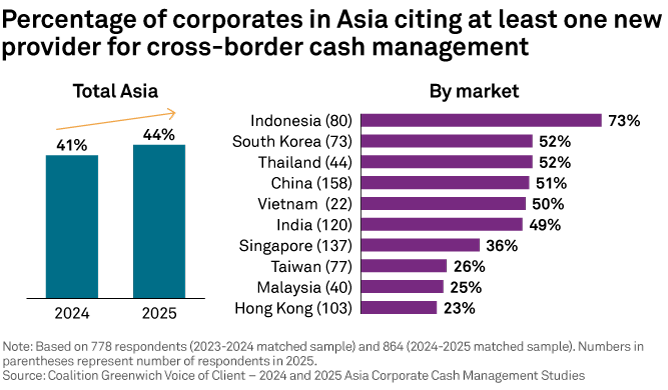

As a result of these intersecting trends, 44% of large corporates in Asia added at least one new cash management banking relationship last year.

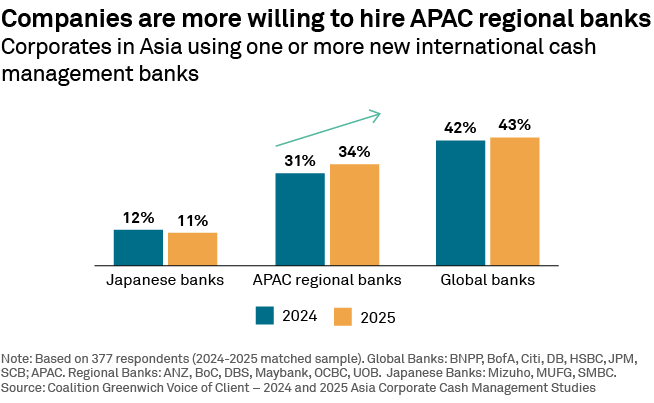

The bulk of these new cash management hires are global banks. Forty-three percent of corporates in Asia that onboarded a new cash management provider last year hired a global bank. However, as shown in the following graphic, a growing share of companies are turning to Asia’s regional banks for cash management services within APAC. These results suggest that Asian regional banks are beginning to compete with global providers on a more even footing within the scope of intra-Asia trade.

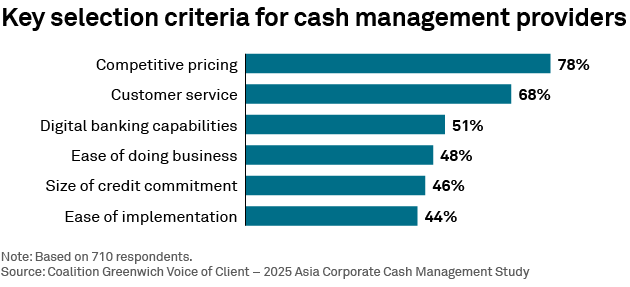

The graphic below provides some clues about why regional Asian banks are increasingly able to compete against global providers within the region. As the chart shows, corporates are paying close attention to factors like digital banking capabilities and ease of doing business.

Asian regional banks have invested heavily in technology. Unlike global providers that must layer new capabilities onto existing legacy technology systems, Asian regional banks have been able to modernize more selectively and execute transformation initiatives with greater agility. This approach has allowed them to accelerate upgrades in their implementation process, connectivity and user experience. As a result, their systems can be relatively easy for corporates to implement, connect to and use.

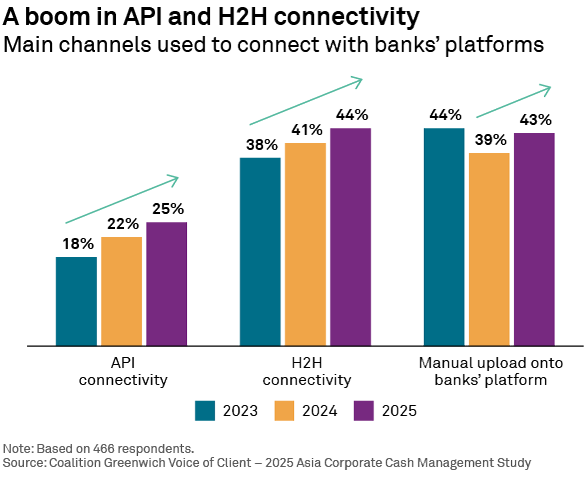

This connectivity advantage is paying off. As shown in the following graphic, the use of APIs and host-to-host (H2H) connectivity is surging among corporates in Asia. Here is how a representative of one large Asian company described it: “Many organizations are adopting a hybrid approach, leveraging H2H for bulk operations and APIs for dynamic, real-time interactions.”

Increased adoption of APIs is the result of a virtuous circle in which banks are building out their suites of connectivity tools to attract clients, corporates are modernizing their internal technology stacks, regulations are creating API standards all sides can rally around, and broader innovation is promoting the emergence of “modular” systems architecture that makes it easier for corporates to “plug-and-play” new tools and applications into their platforms.

The confluence of these trends is making it easier for corporates to connect bank cash management platforms to their own enterprise resource planning (ERP) and treasury management (TMS) systems and onboard new providers. Reflecting that advancement, the share of corporates in Asia saying they plan to implement multi-banking solutions for cash management increased from just 26% in 2023 to 32% in 2025—a sign that this industry is on track to become even more open and competitive in coming years.

Onboarding: Still a headache

At this point, it is important to introduce a critical caveat: Although it’s getting easier for corporates to onboard new banks in cash management and other functions, it is still, by no means, easy. Onboarding has been a traditional pain point for companies and remains one of the main complaints about their banking relationships.

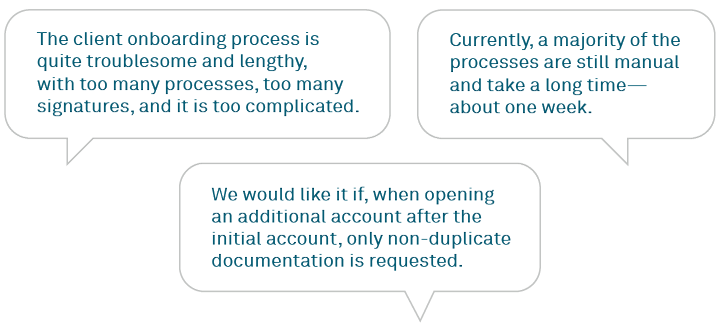

As part of our 2025 Asia Corporate Cash Management Study, we asked 433 corporates in Asia to describe the bank onboarding process and tell us what their banks can do to improve. Here are a few of the comments:

As these comments suggest, the No. 1 request from corporates is for banks to simplify the process and reduce unnecessary steps. As part of that effort, companies want banks to better leverage technology to manage data collection and use, especially in terms of populating documents with data the bank already possesses. As one study participant put it: “Speed is important in opening the account. When we are already part of the system, they should not ask for documentation again. There can be a digital/online tool for e-verification of documents, and the account should open in two to three days max.”

Finally, companies understand that technology is only part of the solution. Corporates in Asia are asking banks to deploy skilled and attentive teams, and ensure that relationship managers respond quickly with support when required. As another study participant concluded, “Let the RM team get involved in the process to make it more efficient.”

Real-time payments enter the mainstream

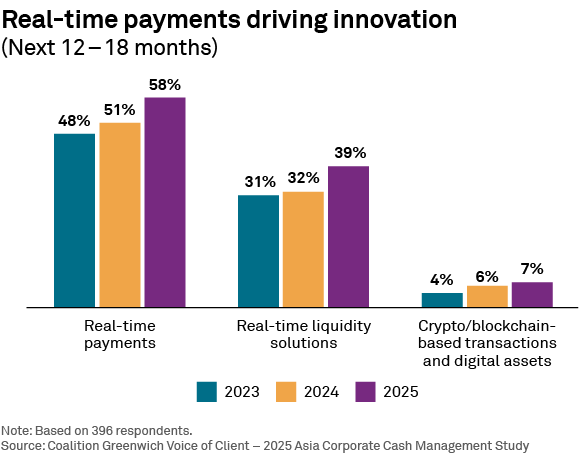

Nearly 60% of corporates in Asia participating in our study expect to be using real-time payments within 12–18 months, and approximately 40% expect to be using real-time liquidity solutions.

The rapid uptake of real-time payments and the gradual adoption of broader real-time liquidity solutions suggest that real-time capabilities have already emerged into a must-have offering for banks competing for corporate cash management business in Asia.

These capabilities are becoming so widely used for domestic cash management that they are beginning to influence companies’ overall satisfaction levels with providers, as evidenced by this comment from a large Chinese corporate: “Our bank offers real-time capabilities, both domestically and internationally, within a T+1 timeframe. It is convenient, without any risks, and why we rate them with high satisfaction.”

As shown in the preceding graphic, blockchain-based transactions and digital assets have yet to materialize in a meaningful way in Asia corporate cash management. However, companies are closely watching the development of digital currencies, digital bridges, stablecoins, and other crypto-related products. They are also aware that banks, especially U.S. banks, are making sizable investments in blockchain technology, and companies are looking to these providers for advice around these potentially revolutionary products.

AI: Investment and ambivalence

According to a 2025 study, Asia is the most polarized global region in terms of artificial intelligence adoption, with a sizable portion of companies that are using AI extensively, and another sizable portion that have zero plans to use AI at all.

In terms of AI investment plans, corporates in Asia are much less ambitious than their counterparts in other regions. For example, nearly 70% of large companies in the U.S. plan to boost their investments in AI. In Asia, that share is less than half.

When it comes to AI offerings from their banks, Asian companies seem largely ambivalent. Companies express real concerns about how banks utilize AI in cash management. For example, companies say they are worried about bias, errors, a lack of consistent regulation, and the potential for banks to replace human client service with AI chatbots. Despite those reservations, only 4% of corporates globally have had a conversation with their relationship manager about AI in banking.

Nevertheless, corporates in Asia are not opposed to their banks leveraging AI. In the end, companies in Asia and around the world care most about the quality of the cash management products and service that banks provide, rather than how the banks deliver that quality.

Ruchirangad Agarwal, Elijah Lim, and Wesley Han specialize in Asia corporate/transaction banking and treasury services.

MethodologyFrom August to November 2025, Crisil Coalition Greenwich conducted 1,288 interviews in large corporate cash management at companies with annual revenues above US$500 million in China, Hong Kong, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. Subjects covered included product demand, quality of coverage and capabilities in specific product areas.