Table of Contents

Banks investing in digital upgrades to cash management platforms should heed one key rule: Corporate clients aren’t interested in stories about how much banks are spending or their latest exciting innovation; they only care about results.

The 1,020 large European companies participating in the Crisil Coalition Greenwich Voice of Client – 2025 Europe Cash Management Study give their cash management banks unimpressive grades for innovation. This finding might seem strange, given the huge sums banks are spending to modernize their platforms in cash management and other key client systems. But for corporate treasury departments, all that effort and investment don’t matter if they don’t have a practical impact on everyday workflows, and if banks don’t pair technology offerings with high-quality, proactive service from human bankers and product specialists.

In this report, we identify the things that really do matter to companies when they assess and select cash management providers. After good pricing, corporate treasury departments are looking for two things: strong customer service and a platform that makes it easy for staff to do business and accomplish essential tasks. Drawing on data from our study, we’ll show corporate treasurers and other decision-makers what actions their peers are taking to ensure banks are meeting their needs in cash management and other essential areas.

Companies unimpressed by bank innovation

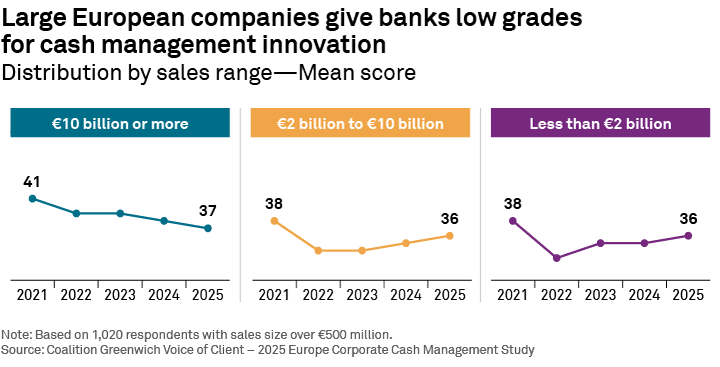

The following graphic shows the ratings large European companies give their banks for innovation in cash management. As the charts illustrate, these ratings were never strong and took a nosedive during the COVID-19 crisis, when many companies felt their cash management providers didn’t do enough to support them and their operations during the lockdowns.

For banks, these low ratings must be frustrating, given the level of attention and resources they are putting into developing digital solutions for cash management. But there is a simple explanation for this apparent disconnect: From companies’ perspective, bank innovations are not improving products and services in the areas that are most important to corporate treasury departments—or at the very least, they are not improving them enough.

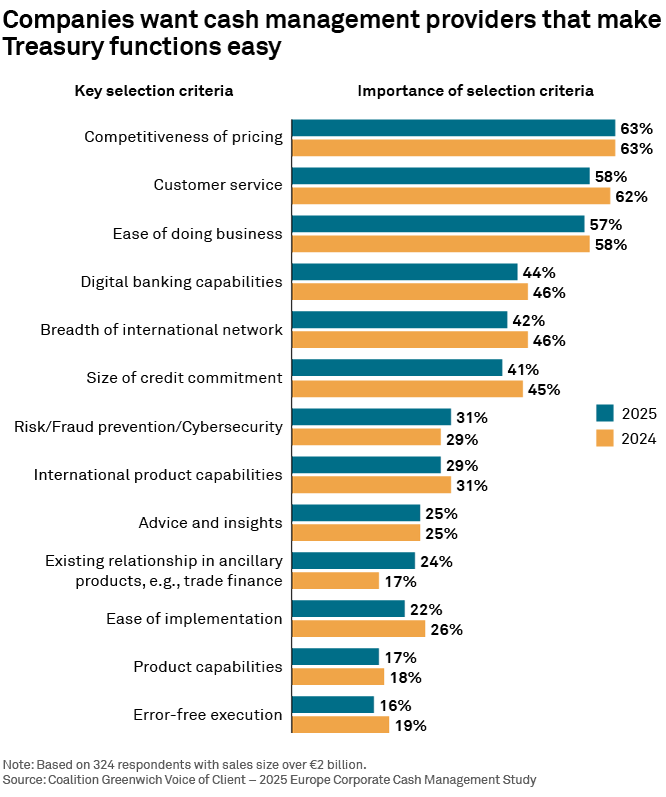

The following graphic shows the top criteria large European companies consider when selecting providers in cash management. As the chart illustrates, the No. 1 factor in these decisions is price. However, ranking just behind price are two closely matched and interrelated criteria: customer service and ease of doing business.

For companies, customer service incorporates a range of expectations about how cash management providers should support treasury staff on a day-to-day basis. The graphic below lists the main factors that influence company ratings of overall service quality. As the chart shows, most of these items reflect the quality and intensity of the coverage the company receives from sales specialists, including how proactive they are in providing advice, how frequently they are in contact, and how responsive and prompt they are to inquiries and issues.

The last factor on that list covers an even broader range of expectations. “Ease of doing business” is a catch-all category that captures how effective banks are at marshaling all their human and technology resources to solve problems and make it easier for treasury staff to execute cash management functions.

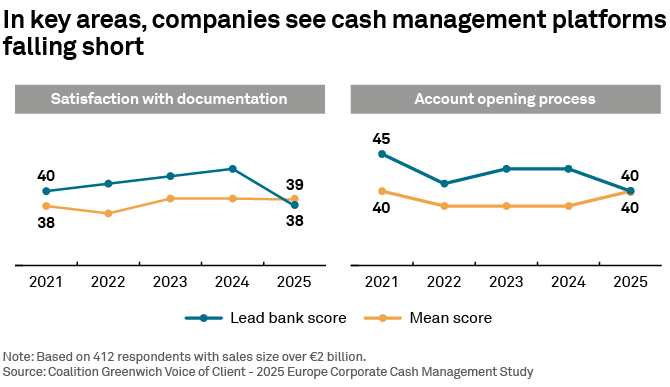

For example, two perennial pain points for treasury staff—and two key components of “ease of doing business” in cash management—are in banks’ effectiveness in account opening and in documentation requirements. It is in these two central tasks that we start to see the origins of companies’ dissatisfaction with bank innovation. As shown in the following graphic, companies give banks sub-par satisfaction scores in both documentation and account opening. And despite years of consistent effort on the part of banks, these scores have not improved since 2021.

Effective innovation supports sales specialists and targets treasury pain points

These findings should present a clear roadmap for cash management providers. When planning investment budgets, banks should be laser-focused on two areas: innovations that help make human bankers more effective, and digital solutions targeting the relatively small number of workflow tasks and issues that matter most to treasurers and their staff.

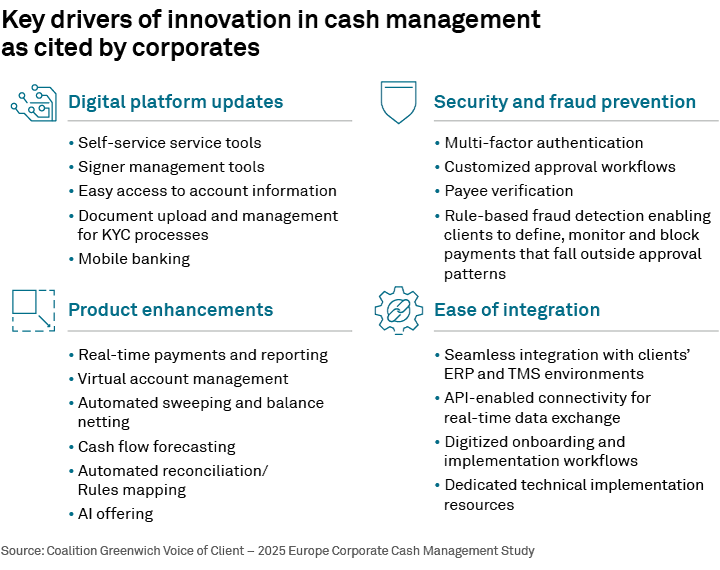

Of course, transformational breakthroughs in artificial intelligence will define the future for cash management and other corporate functions. However, about half of large European companies have not even started implementing AI in treasury departments. For now, treasury staff are far more interested in innovation in basic areas like self-service tools and document management. The following graphic lists key areas in which innovation would truly move the needle for corporate treasury departments in cash management, according to companies in the study.

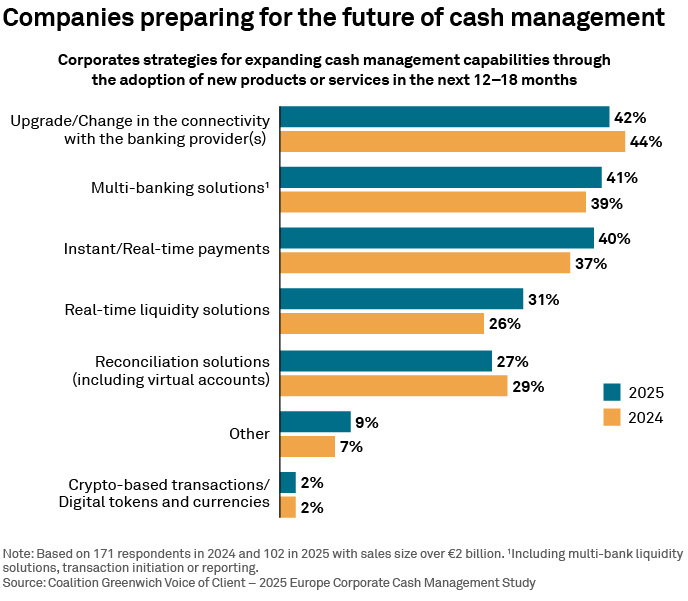

The data also provide important signals for corporate treasurers about the strategies their peers at other companies are planning to modernize and enhance cash management capabilities. Specifically, more than 40% of large European companies are working to expand capabilities by integrating APIs and other technology to upgrade their ability to connect with providers and adopting multi-banking solutions. A similar share is working to establish an infrastructure for real-time payments, which will become universal in the Eurozone this year.

Optimizing bank relationships

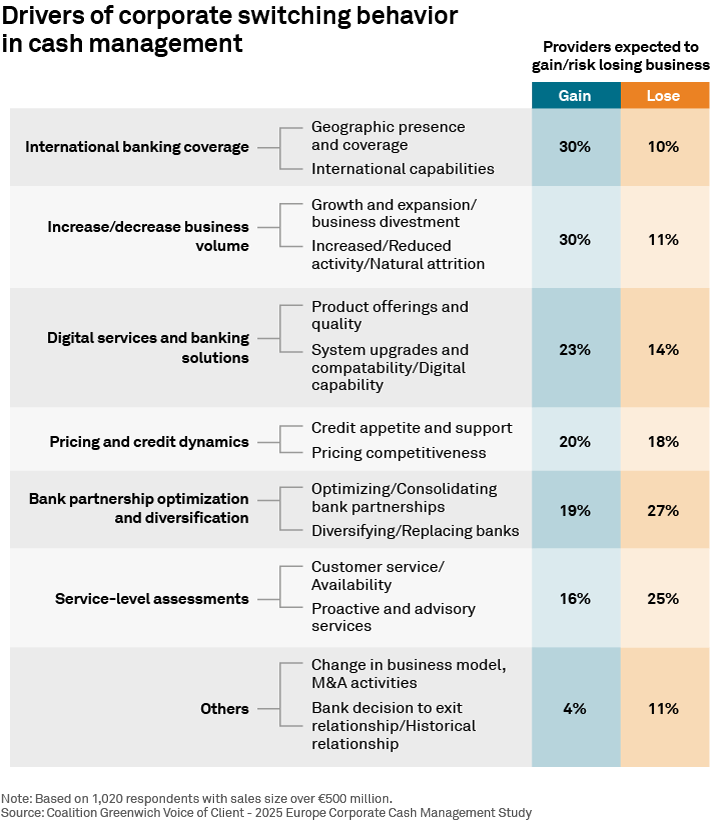

Despite companies’ concerns about bank innovation, service quality and ease of doing business, none of those factors rank as the top reason companies cut business with individual cash management providers. Instead, the main driver of “switching” behavior in European cash management is corporate efforts to optimize bank relationships—a goal that is often achieved by consolidating their business among fewer providers.

Nearly 30% of large European companies expect to reduce the amount of business they do with specific cash management providers due to optimization plans and consolidation.

Of course, some of the consolidation in companies’ lists of cash management providers is not by design. Instead, it’s part of the fallout from mergers and acquisitions in the European banking industry. That has certainly been the case for companies in Switzerland and for companies across Europe that used Crédit Suisse for cash management before that bank’s 2023 acquisition by UBS. Consolidation has also been a fact of life for companies in Spain and other European country markets.

At a broader level, however, European companies are increasingly viewing cash management as part of their broader strategic relationships with banks, as opposed to a stand-alone business. That means they are weighing the value they get from relationships with each provider in the context of the overall level of support they receive from a bank in terms of credit, trade finance, FX, and other banking products and services (see earlier chart, Companies Want Cash Management Providers that Make Treasury Functions Easy). This is, in fact, the criterion that increased most in importance when companies select cash management providers, from 17% in 2024 to 24% in 2025. Based on that assessment, they are moving to optimize value by concentrating business with their most important banks.

That’s bad news for Europe’s local banks, which are trying to compete in corporate cash management with much more limited balance sheets and product capabilities. In fact, Europe’s local banks face a series of headwinds that are placing them at a disadvantage to large banks and global rivals.

For example, when it comes to companies’ selection criteria for cash management providers, breadth of international network now ranks alongside size of credit commitment in importance. With global banks investing massive sums to build out their international networks and improve the quality of their international cash management service in foreign markets, it is becoming increasingly difficult for any smaller bank to compete. The story is much the same in digital capabilities, where the large budgets of global banks will represent a powerful long-term competitive advantage as AI applications start to have a bigger impact in cash management.

Conclusion

Effective cash management service today must be the quintessential blend of human and technology. Large European companies are looking for providers and platforms that make their treasury departments more efficient and life easier for their treasury staff. More than anything, companies want partners that deploy human bankers who understand their businesses, provide prompt and responsive service, and are stepping up proactively to provide advice.

For that reason, banks should continue investing heavily in innovations that make their sales and customer servicing teams more effective—even if those investments are never explicitly recognized by clients. That spending should be complemented by investments in digital solutions targeted narrowly at the most important day-to-day cash management functions and the most frustrating day-to-day pain points for corporate treasury professionals.

For their part, companies should understand that their peers are managing their bank relationships strategically. For these companies, cash management is viewed as just one part of a broader partnership with banks that also include credit and other bank offerings. The goal is to optimize the value the company receives from each relationship, and ensure continued access to credit and other essential products and services.

Across the industry, we believe that effort by companies to maximize value in both specific products like cash management and across broader relationships will play to the strength of global competitors and could contribute to additional consolidation among European banks.

Global Head of Corporate Banking Dr. Tobias Miarka specializes in corporate banking, cash management and trade finance services globally, and Research Director Melanie Casalis specializes in these banking services across Europe.

MethodologyFrom May to November 2025, Crisil Coalition Greenwich conducted 1,020 interviews in corporate cash management at companies in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom. Subjects covered included product demand, quality of coverage and capabilities specific to cash management. Interviews for corporate cash management were with corporates having annual revenues in excess of €500 million.