In an era of “Know Your Customer” and other strict documentation requirements, large European companies are crying out for digital solutions that make it easier for them to do business with their banks. Unfortunately for European banks, U.S. rivals (and HSBC) have opened a commanding lead in these critical digital technologies. That fact is making it difficult for Europe’s banks to defend critical corporate relationships from these increasingly aggressive competitors.

Prior to the global financial crisis, innovation in corporate banking meant the rollout of new and increasingly sophisticated banking products. A decade later, the innovation that companies care most about has less to do with financial products and more to do with electronic systems that make banking operations better, cheaper, faster, and easier—and eliminate “pain points” that have come to define the corporate banking customer experience.

KYC is by far the biggest issue. “KYC is taking an increasingly larger share of our time and resources at our treasury department,” says a participant in the Greenwich Associates 2018 European Large Corporate Cash Management Study.

KYC issues seem particularly frustrating because treasury professionals believe their banks could be doing more to alleviate the burden. As one European corporate treasury professional explains, “It is time-consuming and boring work, and we do not see it giving us any added value. Instead of pushing the work load over onto us, much of the work should and could be done by the banks themselves, since much of the information required is publicly available information, like certificates of registration, with information related to who is authorized to sign for our company and our many domestic and international subsidiaries.”

Another treasury professional echoed those complaints, adding that “Requirements related to AML (anti-moneylaundering), KYC and account-opening processes are out of control.” He continued: “Much seems unnecessary and redundant, as our bank either has received the information from us earlier or could access it from publicly available sites.”

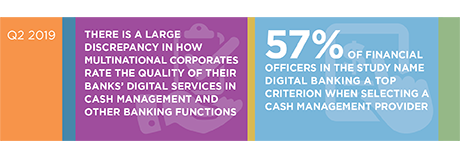

MethodologyGreenwich Associates conducted 2,345 interviews with financial officers (e.g., CFOs, finance directors and treasurers) at corporations and financial institutions with sales in excess of €500 million, including 1,047 with sales of at least €2 billion.

Interviews were conducted throughout Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom. Interviews took place from August to November 2018. Subjects covered included bank credit capabilities, domestic and cross-border advisory capabilities and quality of institution and relationship management. Cash management and trade finance capabilities were examined in separate interviews with corporate treasurers.