New regulatory schemes such as MiFID II, combined with what may be a secular shift to an environment where institutional equity trading volumes may not recover to levels seen even a few years ago, are prompting institutional investors and brokers alike to ask: Who will come out on top?

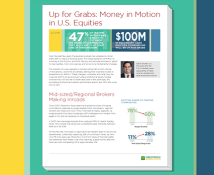

Since 2007, Greenwich Associates has tracked the share of trading commissions captured by bulge-bracket firms, mid-sized or regional brokers and “execution-only” firms. The trend is readily apparent, as bulge-bracket firms face increasingly stiff challenges from smaller firms eager to try and put pressure on the global banks.

MethodologyGreenwich Associates conducted in-person and telephone interviews regarding U.S. equity investing with 223 U.S. equity portfolio managers and 321 U.S. equity traders between November 2015 and February 2016. Respondents answered a series of qualitative and quantitative questions about the brokers they use and their businesses in the U.S. cash equity space.