In July of 2020, the long-awaited SEC Rule 606(b)(3) instituting not-held order disclosures (aka “Institutional 606”) came into final effect. What was not so certain was whether the buy side would actually use the information from these reports or whether these disclosures would lead to meaningful changes. Our research finds that both are likely to occur.

Moreover, in the ever-changing landscape of electronic trading, more data leads to a growing variety of choices in how to trade. Access to these methods is important, but an ability to analyze the results of the outcomes is just as critical. Simply put, the systems that provide the most value are those that can marry access to the wide array of execution solutions to the vast amount of data that such executions produce.

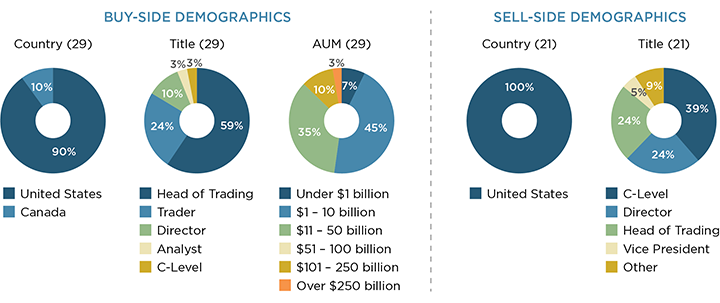

MethodologyFrom May to August 2020, Greenwich Associates interviewed 50 North American buy-side and sell-side firms to discuss Rule 606(b)(3) readiness, plans for using 606(b)(3) data, responses to 606(b)(3) data, use of data to identify liquidity sources, as well as the firm’s management of workflow around liquidity.