Credit markets have come under immense pressure in 2022. A litany of market frictions this year have created new trials and tribulations for corporate bond traders while exacerbating some existing concerns. At the top of the worry list is the need to source liquidity against a backdrop of consistent market volatility. And just when bank counterparties and their capital are needed the most, balance sheets have shrunk and bid-offer spreads have widened to account for new market risks. The knock-on effect is that buy-side traders have lost some of their faith in the market data they have come to rely on over the past decade, with bond prices not behaving as they once did.

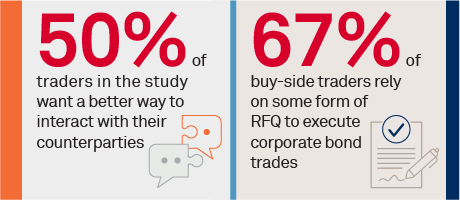

The buy-side traders we spoke with for this study echoed these sentiments. Today’s trading environment just isn’t lending itself to older, traditional electronic trading methods and protocols that have held up well in the past. While request for quote (RFQ) still accounts for over 40% of market volume, that percentage has dropped notably since the pandemic began over two years ago. This research examines these challenges and discusses what actions are being taken to attain a desirable future state in three key areas: the next phase for market data, the role of dealers and their balance sheet and new electronic trading solutions that will help bring it all together.

MethodologyBetween March and May 2022, Coalition Greenwich conducted a series of qualitative interviews with a dozen traders from major buy-side and sell-side institutions in the U.S. Topics discussed included recent challenges associated with sourcing liquidity, given the new macroeconomic regime of higher rates, more volatility, post-COVID impact, and inflation. Additionally, data derived from the Coalition Greenwich 2021 Market Structure & Trading Technology Study based on 30 buy-side participants in the U.S. was leveraged.