The FX industry is no stranger to M&A. Since 2006, there have been 11 major transactions, with the pace only accelerating.

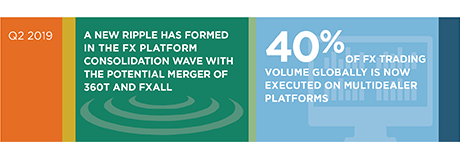

What's interesting about the 360T-Fxall merger is that the two companies occupy a market segment that dominates disclosed trading. In addition, with the uncleared margin rules set to hit users of $8 billion or more in FX Swaps, having a vertically integrated central counterparty clearing house (CCP) will out 360T-FXall in a great position to take share.

MethodologyThis report draws on Greenwich Associates research conducted with 2,369 FX investors globally between September and December of 2018. Respondents were asked to report their electronic trading activity across platforms. In addition, Greenwich Associates spoke with several industry leader to help guide the analysis.