Table of Contents

- 1.AI disrupts research but ignores trading (for now)

- 2.Regulatory reduction simultaneously spurs innovation and creates risk

- 3.Institutional traders figure out prediction markets

- 4.The junk starts washing out of private credit

- 5.Investor benefits from bond-trading venue competition accelerate

- 6.Investors earn yield on chain

- 7.Automation is great, but customer service is better

- 8.The equity market-structure renaissance continues

- 9.Banks and brokers are mindful of disintermediation

- 10.Tokenization finds its killer app

Every year since the 2020 inflection point, the pace of change has felt monumental, and 2025 was no different. Endless artificial intelligence (AI) innovation, a complete change in regulatory posture in the U.S., trading volume records in nearly every market, and economic growth expectations despite bubble concerns made 2025 a year to remember.

The pace of change going into 2026 shows no signs of slowing. Competition between capital markets firms, AI disruption, tokenization, private credit, and an aggressive regulatory agenda will keep everyone busy for the foreseeable future—whether bond and stock prices decide to keep going up or take a pause.

Here are the top things we’ll be watching and expecting in 2026:

AI disrupts research but ignores trading (for now)

New technologies often become overhyped in their early years. AI is not one of them. The hype is real, but while Silicon Valley firms can move fast and break things in pursuit of AI progress, capital markets firms cannot. Instead, they must weigh the balance of the benefits of product innovation against market and reputational risks that could emerge if AI steers them wrong.

As a result, we expect the adoption of AI tools for institutional trading to remain limited among broker-dealers and asset managers in the year ahead. Hedge funds and principal trading firms have long been users of machine learning in their quantitative models, but even among those firms, the actual trading is still generally handled via more deterministic technology.

Research is ripe for AI disruption in 2026. We don’t believe this materializes in the form of GenAI writing automated notes to clients, which is still fraught with risk. Instead, AI is set to help researchers dig into unstructured and private markets data, learn new sectors, find correlations, scrape web and web 3.0 data, and write code to perform analysis that would have taken weeks by hand. Its use will result in better, more unique research with the same number of, or possibly fewer, people.

These tools are becoming increasingly mainstream and are now embedded in major desktop platforms and via newer fintech startups. This research-first approach has also found its way into trade surveillance and market data analysis, which could ultimately provide a bridge to the trading desk. Adoption and access are expected to grow in the months ahead, and we believe AI’s usefulness is only just getting started.

Regulatory reduction simultaneously spurs innovation and creates risk

The excitement about capital markets innovation and growth in 2025 was palpable, compared to the year before. Digital assets, prediction markets, equity and fixed-income market structure, and other items on the 2024 regulatory agenda went from battlegrounds to centers of innovation, as the SEC and CFTC changed their tones under the new administration. A pledge to reduce regulations while also providing clarity in emerging areas has given platform builders and their potential users the confidence to move forward.

But we’d be remiss not to think about the potential for the exuberance to become irrational. Finding the balance between markets that self-police and over-burdensome regulation is notoriously tricky. While most cars can stay on the winding road with no guardrails, consequences are catastrophic for the one that drives a little too fast and goes over the cliff. So, while we’re excited about what we’ve seen in the past 12 months and for what is to come in the next year, we’re keeping a cautious eye out for speeding cars.

Institutional traders figure out prediction markets

A futures contract now exists for nearly anything with an uncertain outcome. Kalshi and Polymarket kicked off the world’s current prediction market obsession that exchange heavyweights CME, Cboe and ICE (which invested in Polymarket) and big brokerage firms (i.e., Interactive Brokers, Robinhood) are now also driving forward.

Some institutional use cases are obvious, such as S&P 500 price targets, M&A outcomes and election results. All can be used to hedge or, more precisely, speculate market movements over time. Others, like Oscar winners and sports winners and losers, are more of a stretch for most institutional investors—hence their appeal to a mostly retail user base. So, what’s next for this emerging market structure?

Institutional market participants and the fintechs that supply them will develop trading tools and strategies to get involved in many, if not all, of these markets. In the short term, trading in contracts with limited financial ties will likely remain the domain of principal trading firms that can provide liquidity for retail investors and generally make a profit on anything with a bid-ask spread. Looking further out, asset managers and traditional bank traders may eventually collect enough historical data to also put these products to use, alongside more obvious financial hedges.

But despite our high expectations for the growth of a market with a nearly limitless universe of potential contracts, it already feels like there are too many trading venues in the United States. Each certainly has a unique take on the market and integration with other parts of the financial ecosystem, which make it attractive. But history has shown that in most instances, one or two contracts tracking the same thing is all that investors need. This suggests to us that consolidation (and some failures) are coming. Whether this happens before the end of 2026 remains to be seen. But regardless of which market center wins, predictions markets are here to stay. You can bet on it.

The junk starts washing out of private credit

Private credit was red hot in 2025. Assets in search of private credit investments flooded nonbank lenders that, in turn, had no shortage of lending opportunities to deploy their cash. And while banks occasionally threw shade at private lending, they were also attracting assets and lending in the private market via credit lines to nonbank lenders or through funds of their own.

Despite the positive benefits of private credit for investors and borrowers, its allure has created a gold rush among less experienced market participants, resulting in inevitably poor investment decisions (see Tricolor) among newer entrants. We expect much of the froth to be cleared from the market by the end of 2026, hopefully via increased market transparency, money-losing fund closures and failed searches for alpha, rather than disastrous blowups and fraud.

Ultimately, these dynamics will lead to a private credit market with fewer gold chasers and more strong, established intermediaries that encourage lending competition, improved access to capital for businesses and new investor opportunity.

Investor benefits from bond-trading venue competition accelerate

We’re no longer talking about the evolving electronification of the bond market—the bond market IS electronic. While buy-side demand catalyzed the move to electronic trading, it was the incredible innovation and investment from competing trading venues over the past decade that made the change possible. That fierce competition keeps innovation coming while driving execution fees lower. Land grabs for portfolio trading, all-to-all, dealer-to-dealer, and even traditional RFQ trading have pushed some venues to offer everything from volume discounts and rebates to fee holidays and prices slightly lower than the competition. But while price matters, diversification by asset class, product, region, execution style, and client type are all key to continued trading venue growth.

Although the result has been great for traders, service providers generally do not like it when competition drives pricing pressure while clients demand more and more. However, a combination of increasing market volumes and nearly inevitable platform consolidation suggests that the number of competitors will shrink while the total pie gets bigger, leaving plenty of market share for everyone as the customer experience continues to improve.

Investors earn yield on chain

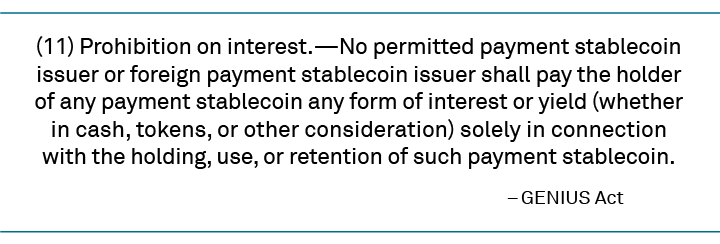

Stablecoins gained momentum in 2025 when the GENIUS Act provided clear guidelines for the on-chain movement of dollars. Stablecoin issuers, including banks, became more comfortable moving forward in the U.S. without fear of regulatory retribution, while the lingering concerns of both institutional and retail stablecoin users (i.e., transparency into the underlying assets) have somewhat subsided.

But stablecoins still leave something to be desired. Most stablecoins do not and cannot pay traditional interest as a bank savings account can. Stablecoin issuers make money from investing user’s dollars into cash-like instruments and collecting the interest while providing its holders easily transferable on-chain cash. But for institutional and retail users looking to store cash balances on chain, the lack of traditional interest payments makes stablecoins akin to putting digital money under a digital mattress—something no financial expert would ever advise.

Tokenized money market funds and tokenized U.S. Treasuries already exist, and growth in the year ahead is inevitable. We do not expect institutional or retail investors to suddenly transfer their cash from traditional money market funds into a tokenized version in a digital wallet. However, many digitally native Gen Zers will create their first and perhaps only investment account in the crypto brokerage ecosystem, and their extra cash will need to go somewhere other than Bitcoin. And for institutions looking to grow their crypto investing or trading strategy, earning interest on cash balances yet to be deployed is key.

Automation is great, but customer service is better

Everyone is trying to automate as much as they can these days. The rational is obvious—doing more tasks faster with fewer resources should equate to higher profit margins. With AI use on nearly every business leader’s annual scorecard, and the technology and executive backing needed to make automation a reality, the potential benefits of true automation for mundane yet mission-critical processes are huge.

More importantly, this evolution isn’t just about improving profitability. Product and service users like automation too, because it often means better solutions and faster access to what they pay for, whether that’s data, advice or collateral reconciliations. But, and this is a big “but,” if something breaks or if you simply can’t figure out the technology yourself, great support, including quick access to informed people, is still often what drives buyers to use one provider over another. So, if you’re saving money by automating parts of your product or service with AI, make sure to deploy at least some of that savings to upgrading or upskilling your client-facing staff.

The equity market-structure renaissance continues

The SEC is moving quickly to ensure the U.S. equity market structure renaissance continues. The commission is reviewing legacy regulations, such as the Order Protection Rule, embracing tokenization and distributed ledgers, streamlining processes across multiple regulators with “mutual recognition,” and promoting the idea of “innovation exemptions” for next-generation technologies.

The SEC’s more creative and collaborative approach should foster continued growth in, and greater competition among, innovative offerings benefiting all participants. For example, AI-enhanced trading venues, algorithmic strategies and analytics platforms should lead to significant improvements in market efficiency via better liquidity sourcing and reduced execution costs. Liquidity itself, long a complaint among institutional investors, could even increase with the rise of tokenized securities and distributed ledger technologies. Along with the potential 24/7 trading, these innovations could attract a broader range of investors and provide more liquidity-sourcing opportunities.

The Commission will need to find the right balance between encouraging innovation and ensuring market stability and investor protection. But under this new regime, equity markets are likely to become more efficient and liquid, fostering a vibrant ecosystem with a diverse range of participants. The renaissance continues, with technology playing a central role in shaping the future of equity market structure.

Banks and brokers are mindful of disintermediation

Competition between broker-dealers has been fierce for hundreds of years. Competition today is coming not only from peers, but from a diverse set of fintech and nonbank entities as well. The impact of nonbank liquidity providers on the trading landscape is nothing new, and the impact of these increasingly large firms is only getting larger. Looking ahead, we see new lines of battle emerging, separate from the world of electronic market making.

Regulatory changes to capital, clearing and collateral have resulted in significant changes to the economics of the derivatives business. Brokers and their clients have changed their trading behavior and looked to optimization tools to blunt the effect of these new costs. Those efforts helped mitigate increased costs but also left open the possibility that other strategies would emerge to absorb this trading and clearing capacity.

Self-clearing could disintermediate banks from their traditional role in derivatives markets. For those investors with the tech and operations staff to take on the task, and also the ability to prove the ROI, the opportunity is notable. But self-clearing isn’t for everyone. Many on the buy side will resist this DIY approach due to the inherent complexities and the view that clearing is not a distinct service—rather, one that is bundled into their broader bank relationships.

Self-clearing was on the table when swaps-clearing mandates descended on the market a decade ago, but mostly fizzled out in the proceeding years. However, technological advancements and regulatory changes have made self-clearing an increasingly real threat to intermediaries worldwide.

Tokenization finds its killer app

The tokenization conversation is at least 10 years old, but it only now seems that the market is close to finding its first killer app. While tokenization could prove to be the perfect technology solution for private equity, real estate and other illiquid assets whose processing infrastructure remains largely manual, its impact on those industries in the short term remains muted. Tokenized, high-quality collateral, however, is shaping up to be a 2026 game changer.

Moving highly liquid U.S. Treasuries and similar cash equivalents on chain allows asset transfers to settle in minutes and unwind in hours, versus overnight and over weekends via the market’s current infrastructure. This newfound speed can prove critical in times of market stress (intraday margin call, anyone?) and when trading outside of normal U.S. banking hours. Already fast-trading markets want to move faster.

Which brings us to 24/7 trading. While the utility of the expanded trading hours is hotly debated among institutional market participants, preparing for around-the-clock trading is a must. Although some might be OK with pre-funding margin accounts on Friday for weekend trading, most won’t want to tie up funds unnecessarily. That’s where tokenized collateral comes in.

Dan Connell, Kevin McPartland, Stephen Bruel, Audrey Costabile, David Easthope, Jesse Forster, Kevin Trimble, Nitin Agicha, Kajal Dubey, and Neha Jain comprise our Market Structure & Technology team.