Private infrastructure remains a popular choice for trading technology workloads, with 53% of firms leveraging private infrastructure on premise, despite the growing attention paid to public cloud infrastructure.

Our research shows that both cost and latency requirements play a crucial role in infrastructure decisions for both buy- and sell-side firms. While we believe that cloud may become the ultimate choice for post-trade infrastructure, front-office trading is managed differently. Non-latency-sensitive workloads, such as research and compliance, are often handled by on-premise private infrastructure. However, emerging artificial intelligence (AI) workloads are influencing infrastructure decisions, with some firms opting to deploy AI in house rather than outsourcing to cloud providers.

We see firms taking a nuanced approach to trading infrastructure decisions, balancing cost, latency and control. For example, larger sell-side firms are adopting a multi-cloud strategy, with two-thirds varying their cloud strategy by asset class, while the buy side often leverages a single cloud service provider (57% have a consistent global cloud strategy).

A hybrid approach, combining on-premise private infrastructure with private colocation and public cloud infrastructure, is a popular method. This allows firms to balance cost, latency and control, and is particularly relevant for sellside firms managing multiple asset classes and latency-sensitive workloads. We believe this is likely to continue, with firms adopting a range of infrastructure strategies to support their trading operations. For instance, a firm running private infrastructure could concentrate about 80% of their workloads on that deployment method but may still put 20% into the cloud.

Looking ahead, we believe that capital markets workloads will slowly evolve until the trading environment shifts further. While cloud will continue to be popular for flexible latency workloads, private infrastructure will remain a favorable choice for latency-sensitive and low-latency workloads. AI evolving rapidly and threatening to move into trade execution could speed up the process of change over time. As AI workloads continue to grow, firms will need to adapt their infrastructure strategies to support the increasing demand for processing power and data storage.

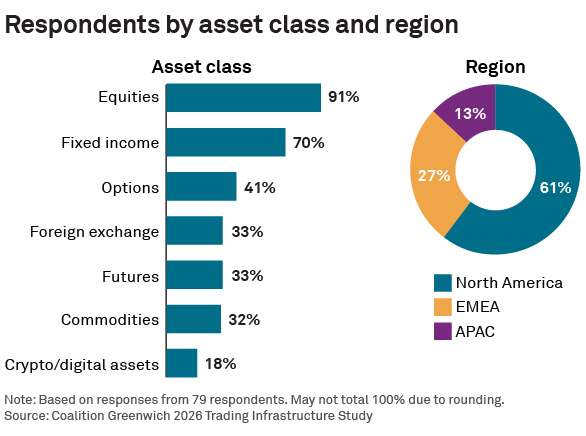

MethodologyCrisil Coalition Greenwich, in partnership with Equinix, embarked on a multi-asset study in North America, the U.K./Europe and APAC on the future of capital markets infrastructure across the trading life cycle. The purpose was to examine how firms deploy private infrastructure, leveraging cloud service providers, managing SaaS and on-premise applications, and distributing AI/ML workloads.

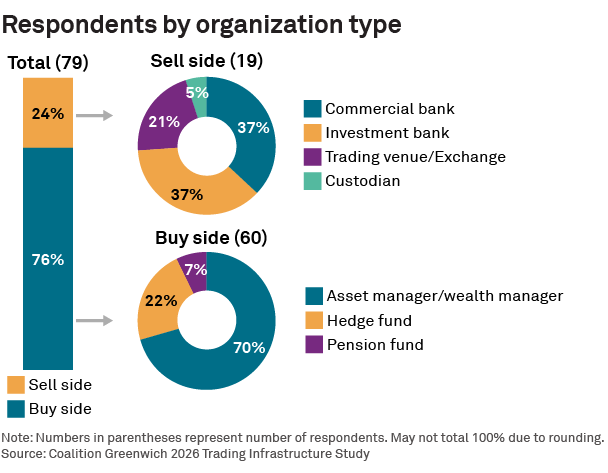

Between October 2025 and December 2025, Crisil Coalition Greenwich gathered responses from 79 companies, including 60 buy-side firms comprising asset and wealth managers, hedge funds and pension funds. Insights were also obtained from 19 sell-side firms, including commercial and investment banks, custodians, and trading venues/exchanges. The respondents were all well-versed in trading infrastructure decisions and comprised front-office professionals.

The insights stem from roles including front office technology and trading experts across a range of asset classes including equities, fixed income, FX, commodities and derivatives.