Table of Contents

Asset management AUM continues to grow at a steady clip. However, that positive trend is providing little comfort to asset managers who have watched profitability plateau. Across the industry and around the world, asset management profitability is under pressure from the long-term trend of fee compression, which in turn is a function of fierce competition between managers, the rise of low-cost passive strategies and the general commoditization of investment “beta.”

Given these conditions, we are confident that the single, dominant trend in asset management in the year ahead will be the quest for manager profitability. This trend will take many forms, in virtually every function and segment of the industry.

In this paper, we will project how the drive for profitability will play out in asset management marketing, sales, customer service and experience, product offerings, budgeting, and cost control, and other key areas. Across these categories, we believe the quest for profitability will manifest itself in 2026 in the form of five strategic initiatives by asset managers around the world:

- Balancing the need for scale with the need for differentiation

- Establishing rigor and precision in the sales process

- Prioritizing, modernizing and enhancing the client experience

- Finding the optimal product mix

- Controlling costs across the business

1. Balancing the need for scale with the need for differentiation

In 2026, asset managers will work to strike the right balance between building efficiency through scale and establishing themselves as differentiated, premium providers.

The most fundamental challenge facing asset managers today is the commoditization of public markets. The rise of passive strategies, combined with the inability of many active managers to deliver long-term outperformance, has fueled a steady compression of management fees. In highly liquid products like equities and investment-grade bonds, where low-cost index funds have proliferated, the most logical path to profitability is scale.

That reality has been a driving force of industry mergers and acquisitions (M&A) for over a decade. In recent years, managers have worked to enhance the benefits of scale by merging individual brands, boutiques and affiliates into a single, unified distribution platform that lowers costs and allows individual salespeople to “sell the entire firm.”

However, that drive for scale can often conflict with another profit imperative: The need to communicate a differentiated value proposition that maintains pricing power and, in the best of cases, charges investors a premium.

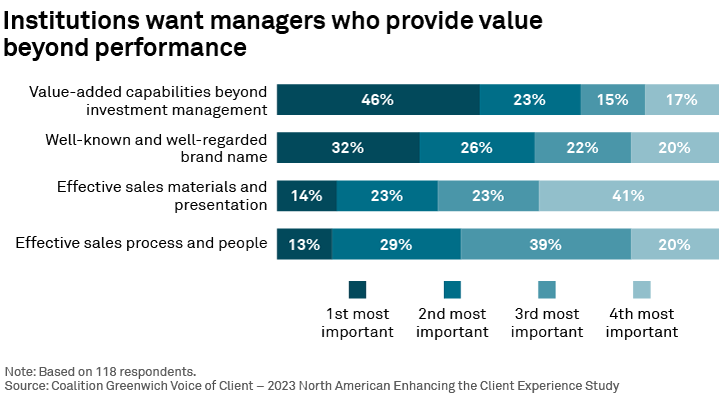

Institutional investors do not select managers strictly on performance. As illustrated in the following graphic, institutions gravitate to managers who demonstrate value-added capabilities beyond pure investment management, as well as those with well-established brand names.

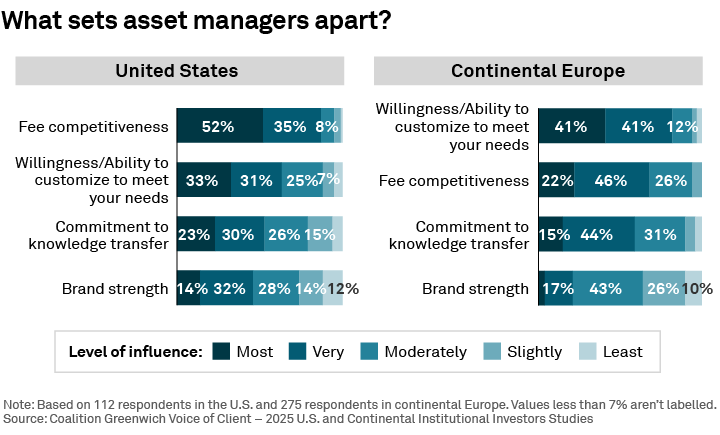

The next graphic goes even deeper, looking at the specific value-added capabilities institutions prioritize when they select their managers. As the charts show, asset owners place a high value on things like a manager’s ability to customize offerings and their ability and willingness to share intellectual capital.

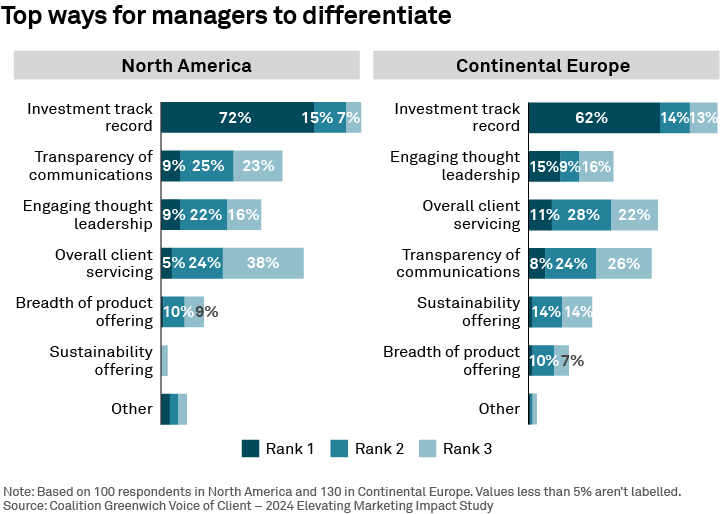

These findings show that managers can derive real competitive benefits by communicating a value proposition that clearly differentiates them from rivals in ways that matter to institutional investors. The graphic below shows the top three ways managers can differentiate themselves based on direct feedback from institutional investors. While investment track record is the most compelling differentiator, managers can also set themselves apart with superior thought leadership, client service and communication.

Within those buckets are virtually endless potential variations. Asset managers have successfully differentiated themselves based on deep knowledge of a particular institutional/client segment, unique product offerings, customization, sustainability, culture, and other attributes.

2. Establishing rigor and precision in the sales process

In 2026, asset managers will use data analytics and technology to increase the sophistication of their sales strategies in a drive to optimize results.

Artificial intelligence (AI) and other innovations are giving managers the unprecedented ability to analyze the universe of prospects and clients to identify and target the best opportunities for sales. Using unique data analytics and technology solutions that can analyze institutions’ investment history, preferences, attributes, objectives, and perceptions of competitors, these tools can pinpoint those that are best aligned with an asset manager’s value proposition. Coupled with smart content marketing and thought leadership initiatives, these technology tools can provide sales teams with a steady stream of engaged prospects and verified leads. By focusing sales efforts on the best of these warm prospect leads, managers should be able to increase their win rates, while cutting back on time wasted on dubious prospects.

This information is becoming critical for sales teams as asset managers ramp up product development efforts as a means of keeping up with investor demand and maintaining or expanding profit margins. This continuous experimentation and expansion of the product slate will increase pressure and time demands on sales teams, who more than ever will need unique data analytics and technology solutions that make them nimble and effective enough to keep up.

3. Prioritizing, modernizing and enhancing the client experience

We believe 2026 will be the year that institutional asset managers fully embrace the client experience.

Until relatively recently, some institutional asset managers paid little to no attention to the concept of the client experience or the client journey. In fact, in the not-so-distant past, these managers paid only minimal attention to client service at all, on the assumption that performance and other attributes of the investment function would drive sales and asset retention.

Things could not be more different today. Facing steady fee and margin compression and fierce competition for assets, managers are pulling every available lever to build and strengthen relationships with clients. That includes providing clients with the best possible experience at every stage of the relationship, starting with prospecting and sales.

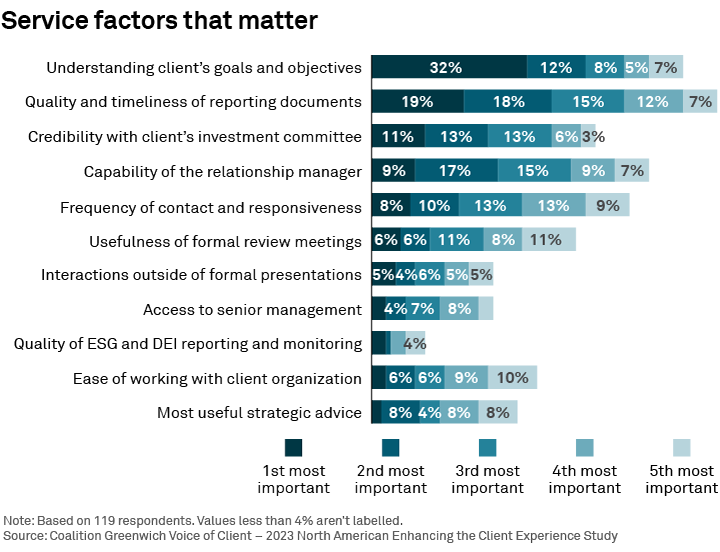

To do so, managers will adopt new client service strategies and invest in a host of innovative technology solutions designed to enhance client experiences. The preceding graphic shows the many service elements institutions say contribute to a top-quality client experience. To measure progress, identify vulnerabilities and ensure improvement, asset managers should independently benchmark client perceptions of these factors and the overall experience against industry standards and results from best-in-class competitors.

A commitment to the client experience can have a direct and meaningful positive impact on profitability—if managers approach the issue strategically. For best-in-class firms, the customer experience function is not just a tool for keeping clients satisfied with the status quo. Instead, these firms view the client relationship as a journey and use their CX process to advance clients to deeper and more profitable stages. The goal is to strengthen the relationship over time by consistently meeting or exceeding client expectations and providing added value wherever and whenever possible. The ultimate objective: Achieving the status of strategic partner.

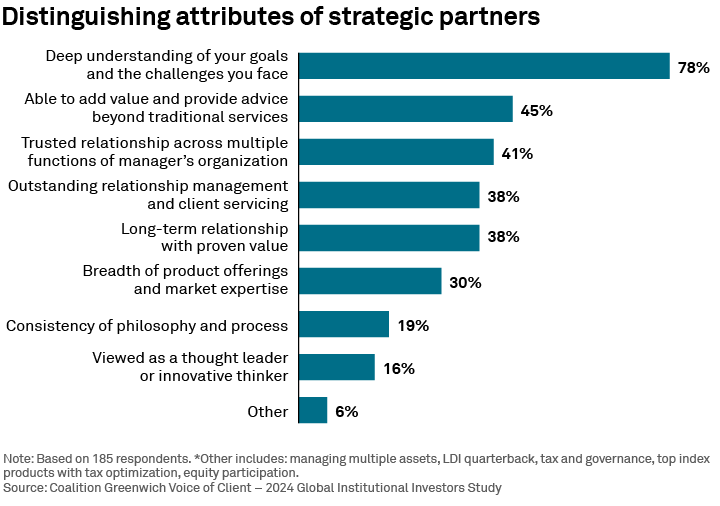

The graphic above shows characteristics managers must demonstrate to be considered strategic partners by institutional clients.

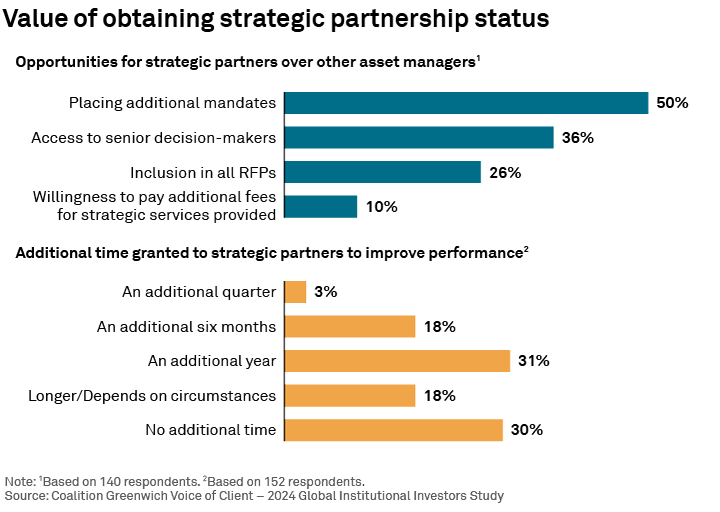

Managers who achieve the status of strategic partners derive benefits that can have a real impact on revenues and the bottom line. As shown in the following graphic, institutional investors say strategic partners receive additional mandates, access to senior decision-makers and other key benefits—including, in some cases, a willingness to pay higher fees. In addition, about 70% of institutions give strategic partners extra time to address periods of underperformance, including about 30% who say strategic partners get an extra year before being put on review.

4. Finding the optimal product mix

In 2026, asset managers will embrace the mantra that not all AUM are created equal.

Over the past several years, asset managers have looked to tap into investor demand for higher returns and boost their own bottom lines by launching active ETFs and other public products that fall between index funds and actively managed funds in terms of fees.

That trend will continue in 2026. However, it will likely be overshadowed by an even more powerful trend driven by the same desire for alpha on the part of investors and higher margins on the part of managers.

Across the asset management industry, passive assets now represent nearly 30% of assets under management (AUM) but account for only 7% of revenues. Meanwhile, alternative assets, which make up just 18% of AUM, generate 57% of industry revenues. These statistics show clearly that some dollars under management are worth far more than others when it comes to revenue generation.1

Given that reality, asset managers of all types will continue adding private markets to their offerings, whether by building private investment capabilities in house, partnering with a private market specialist or acquiring a private market manager. The growth of private market offerings will have a noticeable impact on the operations, sales, distribution, reporting, and client service functions of traditional multi-asset managers.

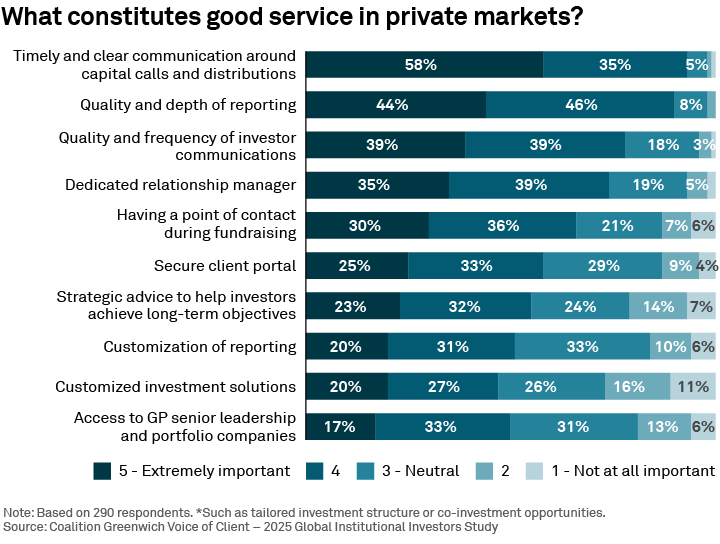

The graphic above shows the services viewed as most important by investors in private markets. Asset managers establishing a private markets business will have evidence of a high level of content knowledge and transparency in areas such as communicating on capital calls and distributions and other unique reporting challenges, and they will have to train up their relationship managers to provide high-quality service and advice on private markets.

Asset management senior leaders will spend the year wrestling with even more complicated strategic questions, such as the extent to integrate public and private distribution, and how to effectively incentivize sales teams in a way that drives sales in private markets while balancing the need to sell traditional products. Finally, asset managers will have to determine how to position their brands to best compete in private markets, where some institutional investors continue to demonstrate a clear preference for dedicated private specialists over even the most powerful multi-asset brands.

5. Controlling costs across the business

Growth in higher-margin private markets won’t be enough to alleviate broader asset manager profitability pressures. Managers will also have to arrest, or at least slow, margin compression across their public-market product slates by improving their operating models and reducing costs.

Rising operating expenses present a challenge for the entire industry. While virtually all managers are affected, the impact varies widely across firms, and increasing costs represent a particular problem for firms with certain business models and product mixes.

Rising costs are being driven by a range of factors, including fast-growing technology expenses that are affecting nearly every company and industry around the world. However, within asset management, several key factors are helping accelerate the increase in operating expenses:

Essential upgrades: Asset managers are spending heavily to upgrade internal systems, including data management and governance, CRM and distribution enablement, client reporting and digital experience/digital portals. In some cases, this spending is critical to address past, chronic underinvestment in the infrastructure that supports core functions. In others, especially data management and governance, the spending is a necessary component of long-term strategies to leverage AI and other technology.

The shift from generalist to more specialist sales approaches: As asset managers look to grow revenues and assets by enhancing the effectiveness of their sales function, many firms are moving from generalist to specialist strategies. In so doing, they are working to establish deep expertise within specialist sales teams that are better positioned to capture money in motion from their focus segments. These teams are usually dedicated to global financial institutions, insurance, ETFs, and in some cases, private markets. Although this initiative is core to long-term growth strategies, it is also expensive in the short term, increasing staffing costs in distribution and elevating firmwide compensation expense.

Creation of data-driven sales teams: Hand-in-hand with the shift to specialist sales strategies, best-in-class asset managers are already generating a tangible competitive edge by leveraging analytics to create a more efficient opportunity pipeline. These managers aren’t necessarily employing AI—although that’s coming soon enough. Instead, they are synthesizing multiple internal and external data sources into timely digestible data and putting this into the hands of sales teams via the CRM.

The rest of the industry is working to duplicate and expand on this success. Almost 80% of managers participating in the Coalition Greenwich 2025 Distribution Effectiveness Benchmark Program have created a dedicated analytics/BI team within distribution, with some following a centralized/generalist approach and others deploying a mixture of data-driven specialist teams within sales, marketing and product areas. Again, this investment is essential to long-term growth but is driving up costs today.

Customization creep: Institutional clients are demanding a level of customization in mandates and service that would have been unthinkable just a decade ago. A combination of technology innovation, product development and increased commitment to the client experience across the industry puts managers in a place to deliver it. However, meeting that demand for customization can be incredibly expensive, and these costs have a tendency to rise over time. Sales teams have an understandable incentive to overpromise or agree to client demands or requests for customization. If managers are not diligent, customization creep will increase both costs and operational complexity. To battle customization creep and hold down costs, managers need to deploy disciplined decision-making frameworks based on strategic KPIs that determine which clients get which customization features.

Asset managers’ success in managing costs while successfully investing and executing long-term growth strategies across all these areas will be a key determinant of the industry’s ability to slow and reverse margin compression in the years to come.

Mark Buckley, Parijat Banerjee, John Feng, and Emma Haffenden-Back authored this paper.

1Oliver Wyman, Morgan Stanley Research estimates from Recalibrating for an Ageing and Multipolar World.