Table of Contents

Under increasing pressure to fund growing liabilities, European pension funds and other institutions are taking action to optimize portfolio allocations and enhance investment returns. As part of that effort, they are reducing holdings of bonds and actively managed equities in favor of real estate, private debt and equity, and other alternative asset classes, and they are asking asset managers for customized offerings to help manage resulting complexity.

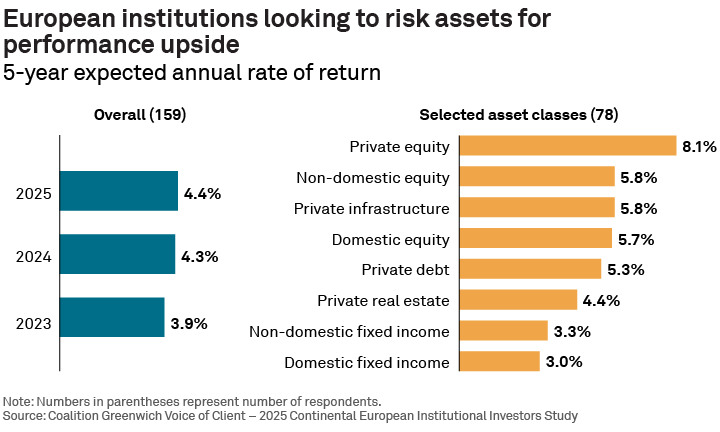

The changing nature of European institutional portfolios can be seen in reported return expectations. As recently as 2023, the expected rate of return (ROR) on European institutional assets averaged 3.9%. By 2025, those expectations had increased to 4.4%.

That dramatic increase in ROR expectations doesn’t necessarily reflect bullishness about future investment market direction. Rather, rising return expectations are being driven by the changing composition of institutional portfolios and the liabilities for which they are responsible.

Throughout Europe, average allocations to fixed income have fallen from post-COVID levels of about 61% of total assets to 58% in 2025. Although those averages span a broad range of portfolio types—with fixed-income allocations ranging from 71% in France to 24% in the Nordics—the directional trend is consistent across the Continent. Institutions that have the flexibility to adjust allocations are moderating fixed-income exposure and adding risk assets to increase potential portfolio returns.

The trend of falling fixed-income allocations appears poised to continue or even accelerate based on institutional hiring plans. The share of European institutions planning to hire a new fixed-income manager in the next 12 months plunged to just 5.5% in 2025 from 15.5% in 2024.

Equity portfolios: More passive and global

Average equity allocations declined three percentage points to 18% in 2025, with averages ranging from just 13% in France to 42% in the Nordics. Also over that same period, European institutions were continuing to shift equity assets from active to passive strategies.

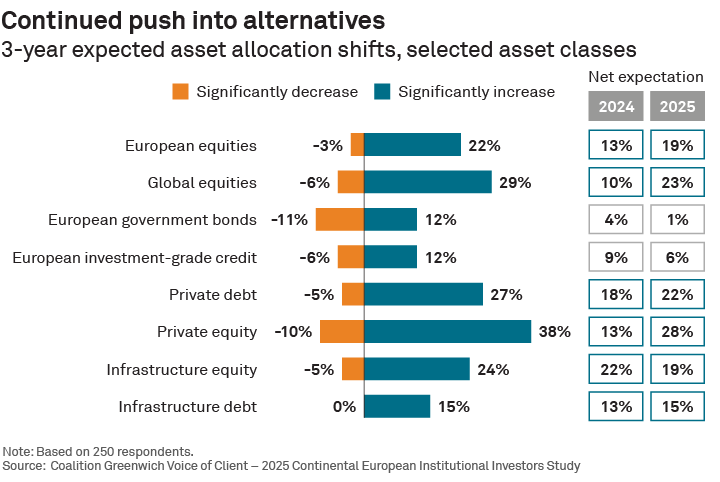

European institutions are also adopting a more global outlook in equities. In 2025, global equities made up 25% of all institutional equity assets, up sharply from just 16% in 2024. As shown in the preceding graphic, European institutions are planning to continue that push into global equities while also increasing their exposure to European stocks.

This shift is likely driven, at least in part, by changing perceptions of the relative attractiveness of European versus U.S. stocks. European stocks outperformed U.S. equities for much of 2025 and have maintained that momentum so far in 2026. A combination of lower valuations on European stocks and a promising outlook for earnings growth based on fiscal spending plans and other tailwinds has increased bullishness about the European market and prompted some institutions to rotate assets out of U.S. equities.

Allocation growth: Real estate and private assets

Assets moving out of fixed income and other traditional asset classes are shifting mainly to real estate and alternative asset classes. Across Europe, average allocations to real estate increased to 7% of total assets in 2025 from 5% in 2024. Institutions report similar growth in alternatives, with average allocations climbing to 11% of total assets from 9% two years ago. At 15% of total assets, alternative allocations are highest in the Nordics and Italy.

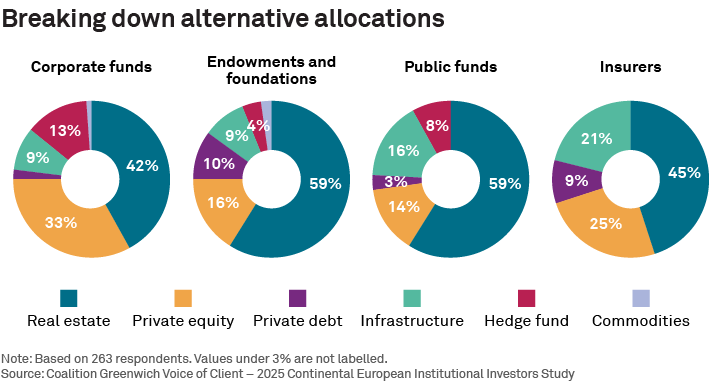

Like their counterparts in the United States and around the world, European institutions are building significant allocations to private equity and debt, as illustrated above. Although real estate remains the dominant holding within alternative portfolios, private equity now makes up roughly a third of alternative assets for European corporate funds, and private debt accounts for approximately 10% of alternative assets among endowments, foundations and insurance companies.

Looking ahead, almost 40% of European institutions expect to significantly expand allocations to private equity in the next three years, and more than a quarter are planning major increases to private debt. Institutions are also planning to meaningfully expand allocations to other alternatives, including infrastructure equity and debt.

Demands for customization

Adding risk assets to a portfolio increases complexity. That’s especially the case with private assets, which come with a host of unique challenges related to implementation, cash flows and risk management, among others.

As rising exposure to risk assets ratchets up complexity, institutions are seeking customized offerings from asset managers that help them analyze and manage their investments in their own way. More than 80% of European institutions cite “willingness/ability to customize” as one the most important criteria they assess when selecting asset managers.

Institutions say customization helps them manage their portfolios more effectively and maximize the value of manager relationships. European institutions specifically cite their growing need for customization in reporting and analysis, which allows for better controls and monitoring, and can enhance portfolio analysis, risk management, compliance, and decision-making. Reporting tailored to an institution’s specific preferences and templates also enables them to more easily compare metrics across managers.

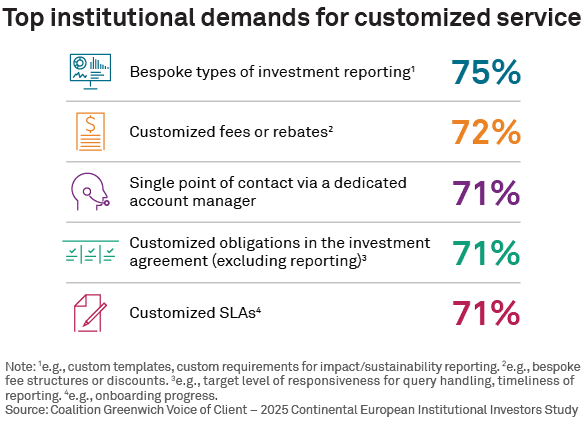

The graphic below shows the services and features in which European institutions most frequently request customization from managers.

More generally, European institutions believe customized propositions from asset managers make them more efficient. “Customized services designed to meet our needs lead to a better, more efficient working relationship,” says the representative of a continental European endowment. A study participant from a U.K. public pension fund agrees: “[Customization] is about the customer being able to operate in the most efficient manner possible. It’s about you having visibility over data in the most efficient manner and having better functionality around the way you look at the data.”

Any institution hoping to receive customized services from their asset managers should understand one important thing: Managers view customization as adding cost. Profit margins for asset managers are under pressure. One driver of margin compression is rising costs associated with “customization creep.” To push back against this increased expense, asset managers are trying to rationalize customization and limit tailored solutions to important clients.

The graphic above shows what institutions are doing to reward their managers for providing customization. As the chart shows, about half of European institutions award additional mandates to managers willing to customize. Another 54% automatically include managers who customize in all RFPs. Finally, 15% of European institutions are willing to pay additional fees for bespoke service.

Mark Buckley and Kryszia Bisson advise our investment management clients in Europe.

MethodologyDuring 2025, Crisil Coalition Greenwich conducted in-depth interviews with 357 key decision-makers at the largest continental European institutional investors.

The 27th annual research study covers the largest continental European corporate, public, and industry-wide defined benefit, defined contribution and hybrid pension funds, banks (including Sparkassen in Germany), foundations and churches, insurance and reinsurance companies, sovereign pension reserve funds and other non-pension institutional investors, including official institutions, central banks, monetary authorities, sovereign wealth funds, and supra-nationals.

For all markets, the institutional investors participating in the study have externally managed assets of over €100 million. This includes larger markets such as Germany, the Netherlands, Switzerland, and France, and smaller markets such as the Nordics, Italy, Iberia, Belgium, Austria, and Ireland. Total assets captured in this research are just over €5.5 trillion.