Table of Contents

With a framework for a comprehensive agreement now in place, large companies in the Middle East are optimistic that local economies and businesses can get back to their previous strong growth trajectories, highlighting the region’s robust economic fundamentals and business resilience.

Given the recent disruptions to business due to the conflict, the International Monetary Fund (IMF) in April had reduced its GDP growth projections for the region by 2.8 percentage points, to 1.1% for 2026. As growth expectations return, this will most likely have a positive impact on any future GDP predictions for the region.

Despite the projected slowdown, on-the-ground observations across the United Arab Emirates and other regional hubs continue to highlight the resilience of economic activity. While oil market dislocations have had mixed effects across energy-producing and energy-consuming countries, the UAE’s diversified economic base has helped sustain overall momentum. Tourism has faced short-term headwinds, though easing travel advisories are supporting a robust recovery in international travel. Across key cities such as Dubai and Abu Dhabi, central business districts remain active, with restaurants and malls visibly busy and business activity continuing at pace, underscoring the economy’s adaptability and resilience.

The IMF seems to agree that the strong fundamentals that underpinned economic growth in the region before the start of the war remain in place. At the same time, it cut growth projections for 2026 and now projects that MENA GDP growth will rebound to 4.8% in 2027. A recovery of that magnitude points to a quick return to the growth trends that have characterized the region for the past five years.

Back to business expansion

What would a quick return to pre-war growth levels look like for companies in the region?

Corporates in the region entered 2026 with a highly positive outlook. Most said they had not been significantly impacted by the U.S. tariffs and trade tensions that had been roiling other economies. Nevertheless, the optimism seen in the early months of 2026 was slightly tempered from the bullishness of recent years, and companies were adjusting their priorities for the year ahead.

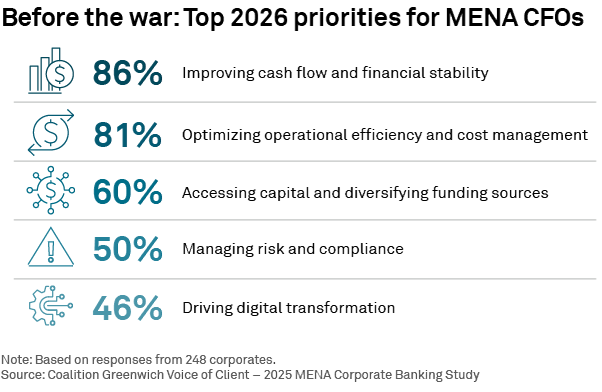

In recent years, corporates in the Middle East have been preoccupied with growth, including both domestic growth and often ambitious international expansion plans. Entering 2026, the companies participating in the most recent MENA Corporate Banking Study from Crisil Coalition Greenwich said their top priorities for the year ahead were improving cash flow and financial stability and optimizing operational efficiency and cost management.

Taken together with the resilient optimism of corporate management teams, this shift in focus suggests that after spending several years aggressively expanding their businesses, companies entered 2026 planning to bolster their balance sheets and focus on operational and cost efficiencies to ensure they have a solid foundation for the next stage of growth. Those plans were upended by the outbreak of the conflict and will have to be recalibrated before normal economic activity resumes and spending on capex sees a stimulus.

The Asia-MENA connection

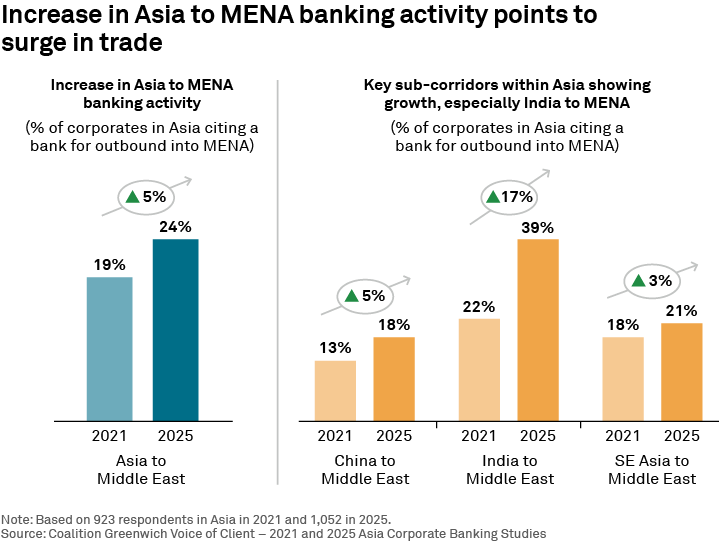

One key driver of MENA corporate growth and economic expansion over the past five years has been the increase in trade between Asia and the Middle East.

Every year, Crisil Coalition Greenwich asks large companies around the world if they employ a bank for any services in different global regions. Since 2021, the share of Asian corporates employing a bank for outbound service into MENA increased from less than 1 in 5 to roughly a quarter (see graphic below). While that increase in activity has been consistent across the region, it has been especially pronounced in India, where the share of corporates using a bank for services in the MENA region jumped 17 percentage points to nearly 40% in 2026.

Over that same period, the average number of banks employed by Asian companies for Asia-to-MENA banking services increased from 1.7 to 2.0, a finding that suggests that companies that have entered the region have experienced a rapid need for increased support, driven by growing business activity.

We believe that trend will resume or possibly even accelerate, as companies in both the Middle East and Asia move to rectify dislocations in supply chains and energy caused by the conflict as well as the ever-changing framework of U.S. tariffs.

Banks are betting that the strengthening of the Asia-MENA trade corridor is a secular trend. As banks from around the world compete for this business, the incumbent international banks are increasingly being challenged by large regional banks in MENA as well as the Asian regionals.

Companies look to banks for efficiency and fast turnarounds, not just credit

Demand for corporate banking services is a reliable indicator for business activity within a region. At the start of 2026, corporates in the Middle East were taking on new bank relationships in both cash management and trade finance. Companies needed more support as they expanded their businesses, both domestically and internationally.

Even as they hired new banks for cash management and trade, MENA companies were not necessarily bringing on new credit relationships. From 2025 to 2026, the average number of banks used by corporates in the Middle East for credit was essentially flat. That stability suggests companies across the region had balance sheets strong enough to finance much of their growth plans.

While the current situation is dynamic, we expect an increase in sales intensity (frequency of contact, responsiveness), as well as a doubling down on customer service by key regional and international banks in the region as conditions slowly stabilize. We believe the business outlook for both companies operating in MENA and banks competing in the region will turn positive quickly as the situation normalizes, and as strong economic fundamentals kick back in, boosted by capex spending.

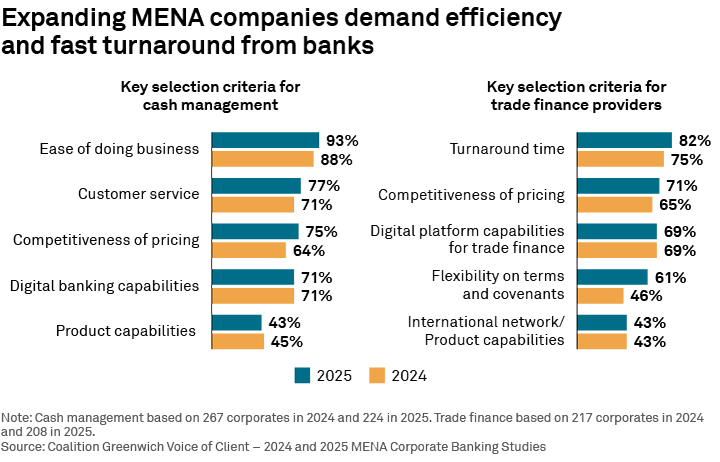

As the economy regains its footing, corporate demand for banking services should accelerate. What will companies be looking for?

The preceding graphic shows the primary selection criteria used by corporates in the Middle East when choosing a bank for cash management and trade finance at the start of 2026. One finding that stands out is the placement of pricing, which—while important—does not rank as the top consideration in either function. This clearly indicates that as corporates focus on their future growth, they demand banking services that will help support it. Those demands are reflected in corporate priorities, with treasury departments listing banks’ “ease of doing business” and customer service as the top criteria when selecting new banks for cash management.

The same mindset guides companies’ thinking in trade finance. With businesses expanding in a volatile global trade environment, treasury departments are seeking banks that are capable of delivering fast turnaround times on a day-to-day basis in trade finance.

We believe that these trends will continue with companies in the Middle East emphasizing high-quality support from their banks over and above competitive pricing, as they look to resume their growth trajectories.

Ruchirangad Agarwal, Amin Shaukat and Pushpak Vanjari specialize in corporate/transaction banking and treasury services in Asia and the Middle East region.

MethodologyBetween September and December 2025, Crisil Coalition Greenwich conducted extensive research across the Middle East, including the UAE, Saudi Arabia, Egypt, Oman, Bahrain, Kuwait, and Qatar. The study comprised 248 interviews in corporate banking, 224 in corporate cash management, and 208 in corporate trade finance.

Participants were senior corporate finance decision-makers such as CFOs, Finance Directors, Treasurers, and Financial Controllers from companies with annual revenues typically of USD 250 million or more.