Financial Transaction Tax Tango

September 30, 2020

By:

Shane Swanson

Table of Contents

Ah, the siren song of easy money—that is what the idea of a financial transaction tax (FTT) conjures up for legislators. After all, the reasoning goes, a small charge added to every securities transaction cannot possibly cause any harm and can only do good. Yes, it is indeed an alluring dream.

Fuzzy Math

Unfortunately, as we have previously written, the stark reality is much different. Those small charges add up to a tremendous amount of real-world dollars, impacting long-term investors, retail traders, as well as the security professionals that provide liquidity to the markets.

In the steps of the FTT tango, individual states are putting their names on the dance card. Back in July, a bill was introduced into the New Jersey Assembly looking to impose a quarter of a cent per transaction[1] on firms that process 10,000 or more financial transactions per year through infrastructure in N.J.

Center of Gravity

Today, much of the U.S. equity market is processed in datacenters located in NJ.

However, the exchanges, the brokers, and the associations that represent them were quick to point out several factors.

First, the mechanics of the markets are far more portable today than at any time in the past. Partly due to the requirement that they have redundancy (with geographic distance), exchanges and other significant market participants have devoted substantial resources towards having the ability to run in disaster recovery centers. Thus, if N.J. were to impose such an FTT, it is highly likely that the industry could move their operations elsewhere.[2]

Although a move would not necessarily be overnight for the industry, other states are likely to actively seek the business that would be driven out by a state-level FTT. Moreover, any imposition of an FTT is likely to accelerate a trend toward moving matching engines to the cloud. When transactions are consummated in the cloud, trying to assign a state-level FTT to individual transactions will become even more of an exercise in futility.

Second, that these taxes do not raise nearly the amount envisioned (because they cause volumes to drop, as well as often causing volatility and costs to increase). As such, it is nearly impossible to plan for the use of proceeds from these taxes because they do not meet the forecasts.

Third, the legality of a state imposing a tax on all security transactions that are processed within their borders would be challenged. For example, if traders in South Dakota and in South Carolina have their trades matched and processed in N.J. and then have a N.J. tax assessed and apportioned completely to N.J., that tax could run afoul of the Commerce Clause and Due Process Clauses. For N.J, in particular, this was sufficient to cause them to drop the FTT from their 2021 budget.[3]

Haven’t We Been Here Before?

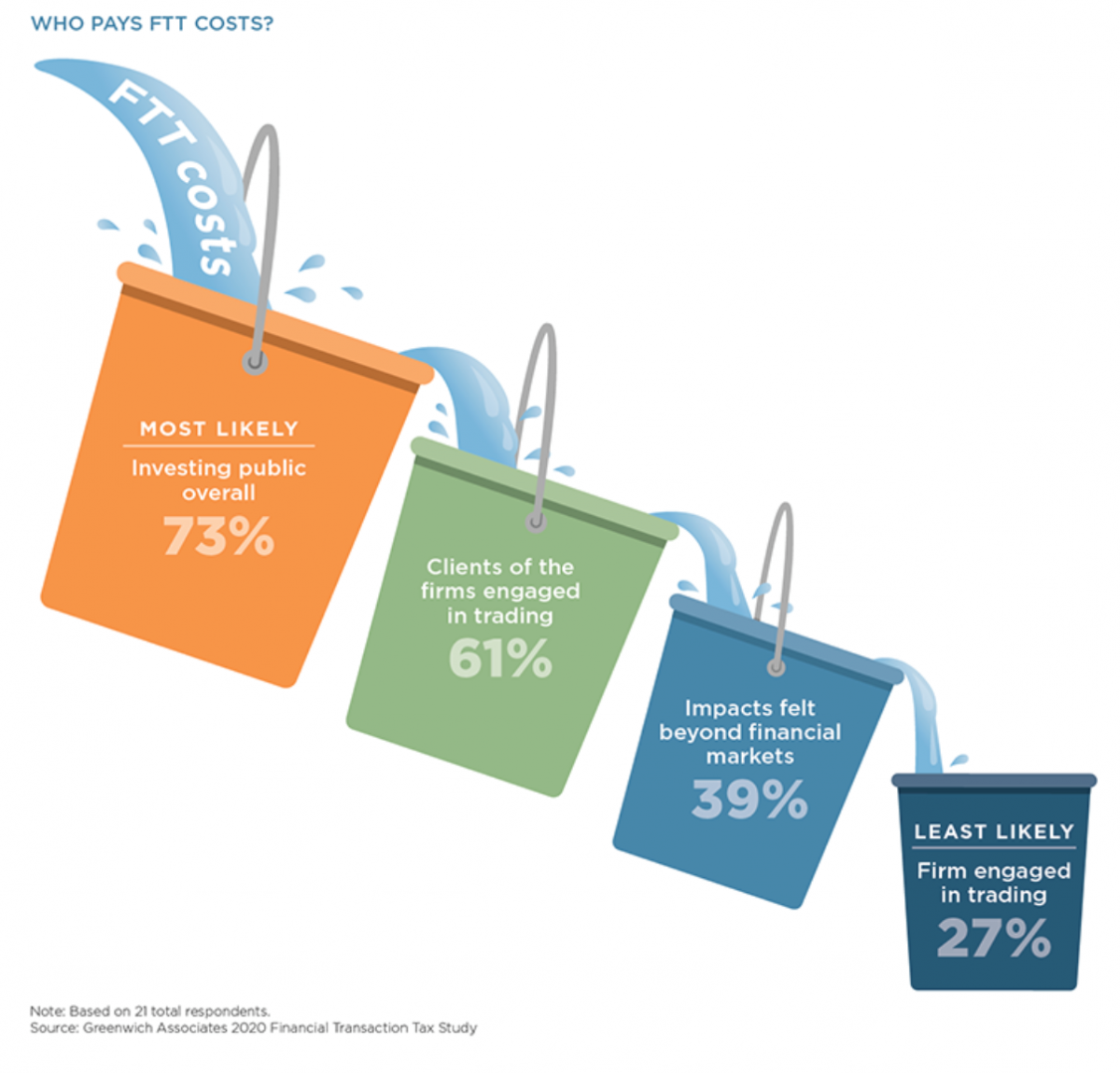

Of course, in particular in this election year, the other possibility for an FTT would be imposition at the federal level. The question remains—who pays for such a tax?

As you can see, when the music stops, and the party is over, the investing public is the one left bearing the brunt of the FTT. So, while states may be thinking about giving the FTT tango a whirl, the data shows that in practice it really has two left feet.

[1] Or possibly per share, depending on how the math gets calculated.

[2] NYSE and Nasdaq have both indicated they would run one of their exchanges from backup datacenters in Illinois. Of course, Illinois has also flirted with the idea of its own FTT.

[3] Although the FTT may be revisited as part of a supplemental revenue proposal.