RFQ use in the global ETF trading ecosystem

Exchange-traded funds (ETFs) are having a moment.

In 2025, total exchange volume for U.S.-listed ETFs soared to a new record of $58.4 trillion, while European-domiciled ETFs also recorded unprecedented highs, exceeding $4.5 trillion. Amid market growth, the request-for-quote (RFQ) protocol has become the dominant trading mechanism for institutional flows, particularly in fragmented European markets.

In this blog, we explore the role of RFQ trading and whether it will have the same staying power in the coming years. Overall, we expect future trading initiatives to hinge on two forces: market structure and market fragmentation. The development of ETF execution technology points toward greater automation, cross-asset integration and the disruptive potential of tokenization. Exchanges and trading venues are expected to continue to innovate to attract volume and win over institutional flow along these lines.

How institutional investors are choosing to transact

This April, U.S. ETF inflows surged to $171.4 billion—nearly triple the amount of April 2025. Looking a bit closer, asset-class splits comprising roughly $14.7 trillion in assets under management (AUM) were mainly equities- (78%) and fixed-income-focused (18%). Likewise, net inflows into European ETFs and exchange-traded commodities (ETCs) increased to EUR 39.8 billion from EUR 8.6 billion in March, with about 60%-65% concentrated in equities and another 30%-34% in fixed income. AUM surpassed the EUR 3 trillion mark.

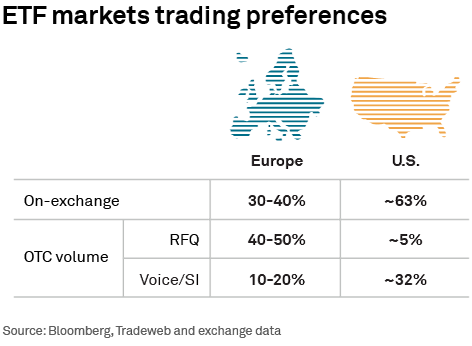

While U.S.- and European-domiciled ETF markets are both attracting more investment, trading preferences are very different when comparing regions. Over-the-counter (OTC) activity using the RFQ protocol leads institutional trading in Europe. Meanwhile, risk transfer in the U.S. is mostly done on exchange or directly through brokers.

Why do these differences exist? There are two primary reasons why institutions are choosing to embrace off-exchange trading using RFQs: market fragmentation and market structure.

In the U.S. markets, the majority of ETF exchange volume is concentrated in about 100 names, including ultra-liquid ETFs like SPY, QQQ, IVV, and VOO. In fact, roughly 30% of the entire notional trading volume of U.S.-listed ETFs is attributed to the SPDR suite of ETFs, with SPY leading that charge. Much of the market’s activity is driven by hedging and short-term trading, which may not align with the traditional definition of institutional flows. Broadly speaking, consolidated, deep, on-exchange liquidity makes the use of RFQs less critical.

Meanwhile, Europe has a unique but fragmented structure featuring several major exchanges (i.e., LSE, Deutsche Borse, Euronext, SIX, Cboe Europe) with multiple listings for ETFs, creating no central source of liquidity. This fragmentation makes it essential to get pricing from market makers who have an aggregate view across all venues—a service not available on a single exchange's order book. As a result, nearly half of all institutional flow occurs through RFQ on Bloomberg’s and Tradeweb’s venues.

Why is RFQ the solution? There are several factors that make the RFQ protocol a powerful tool for managing fragmented ETF liquidity, particularly in European markets:

- Liquidity aggregation: RFQ platforms provide a single point of access to major nonbank liquidity providers, regional brokers and banks.

- Price discovery: They allow investors to access liquidity pools that are larger than the visible depth on an exchange screen, which is critical for executing large or less-liquid ETF trades without significant market impact.

- Market share: Bloomberg and Tradeweb handle the majority of European institutional ETF flow in Europe. Traders are comfortable with the RFQ protocol for other products, making it a familiar choice for ETF trading as well.

- Cost efficiency: Using RFQ can be more economical than trading on exchange due to the disclosed nature of trading (i.e., counterparties have a better understanding of client intentions and can provide tighter bid-offer spreads).

- Best execution: Best execution is a key regulatory driver for using RFQ, as it provides a provable method of sourcing competitive prices.

The evolving ETF competitive landscape: Venues and protocols

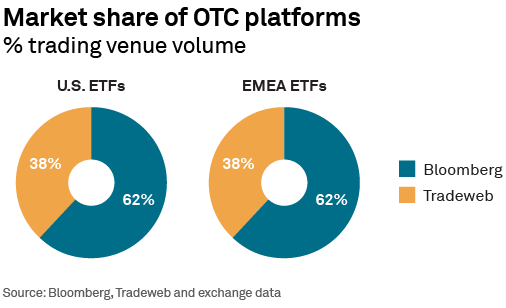

Bloomberg and Tradeweb comprise roughly 60% and 40% of institutional venue trading in Europe, respectively. Bloomberg users benefit from its wide-ranging solutions, integrating portfolio management, analysis and trading tools for a more seamless workflow. Its disclosed RFQ model is seen as a strength for pricing for all ETF types. Tradeweb is known for a strong user interface and access to a wide range of dealers, which is beneficial for less-liquid ETFs. Both platforms enable the trading of adjacent fixed-income products as well.

After acquiring majority control of RFQ-hub in 2025, MarketAxess is reemerging in the institutional space. Backed by a consortium of major market makers (Jane Street, Citadel, etc.), RFQ-hub is a fledgling third competitor operating in the U.S. ETF market. The platform aims to offer lower costs to market makers (which can be passed on to clients) and seamless workflow integration, while also positioning as a multi-asset class platform.

Exchanges have developed counteroffensive plans to attract more flows. Although Bloomberg and Tradeweb are deeply entrenched in European ETF markets, exchanges are keen to develop technology to enhance the lit order book. For example, LSE (RFQ 2.0), Deutsche Borse, Euronext and others have launched their own RFQ platforms. Despite these efforts, these platforms have struggled to gain market share (typically <5% of volume) because they are confined to the liquidity of a single exchange, failing to solve the core fragmentation problem.

As a result, exchanges are now focusing on attracting more retail flow to their lit order books through incentives like free trading, free Level II orderbook depth and specialized “protected” market making. Societal changes in Europe are also enabling more ETF trading. For instance, shifts from bank savings accounts to market-based savings, particularly in Germany, have bolstered growth in the European ETF market. Likewise, longer trading hours that align more closely with U.S. trading have also attracted investment, particularly by younger people investing after working hours.

Exchanges are developing other tools, such as second-generation algorithms, as well. While RFQ and algos still make up a small portion of trading, ease-of-use and cost savings will likely enhance growth and bring more flows to the lit order book in the future. The concentration of more volumes in the closing auction, which has the advantage of transparent fair-value pricing, is also expected to increase and garner more investment from larger institutions.

The future of ETF trading

We spoke to buy-side investors to better understand what development may be in store for ETF markets. We uncovered a few really interesting takeaways:

- A growing push for more automation: Continued reliance on trading venues and the development of more tools on these platforms is emerging. The future of RFQ is rule-based, automated execution integrated directly into order management systems, reducing manual intervention.

- Cross-asset trading: Another developing need relates to integrated trading of ETFs alongside their underlying components (e.g., bonds, equities) in a single basket. Investors are looking for trading platform enhancements to address this need.

- Direct access: There is also interest in changing pieces of the ETF market structure. For example, investors want to bypass the secondary market and create/redeem shares directly with issuers to eliminate trading friction and NAV dislocations.

- Tokenization: Viewed as the next great disruption ("where it's all going"), tokenization is a topic of discussion investors, exchanges and venues are interested in. Although we are still in early innings, firms are already filing for tokenized ETF structures. However, to date, the development of significant infrastructural change won’t happen soon, and regulatory hurdles remain concerning creation/redemption and settlement.

Conclusion

We don’t have a crystal ball. But if we did, we anticipate trading venues like Bloomberg and Tradeweb will likely continue to lead institutional market share in fragmented markets like Europe for some time by offering investors RFQ trading to enhance liquidity. However, exchanges are pushing back by attracting more retail flow through innovation and changing attitudes toward capital markets-based savings and ETFs.

As these forces take hold, more flows are likely to find their way to the lit order book. Overall, we envision a world where investors will look to a combination of trading venues, exchange order books and other tools like algos and automated trading to get the best possible pricing and market transparency.