Treasury tech tools: How companies are innovating to transform treasury operations

In today’s rapidly evolving corporate finance technology landscape, corporate treasury departments are embracing a new wave of modernization, leveraging cutting-edge tech tools to transform how they manage cash, liquidity and risk.

A key driver behind these efforts is the transformative potential of modern AI models, which, when combined with a fundamental overhaul of data governance, create compelling business cases. The advantages that can be achieved fundamentally improve the justification of often significant investments required to improve and restructure data sources, adopt and integrate digital tools—tools that automate processes, boost efficiency and enable powerful predictive analytics—positioning treasury as a vital source of data and strategic insights for the entire business.

To better understand how treasury departments are using and investing in new technology solutions, we surveyed treasury professionals from 142 large companies around the world.

Our analysis of these results yielded three key conclusions:

In this series of three blogs, we attempt to provide insights and guidance to treasurers and other corporate decision-makers by addressing each of these conclusions in detail.

AI has become a core pillar of treasury modernization program

AI is the centerpiece of corporate treasury innovation plans and investment budgets. Our study reveals that after a period of pilot programs and experimentation, sizable shares of global companies have already or are planning to deploy AI solutions in their treasury departments in the coming year.

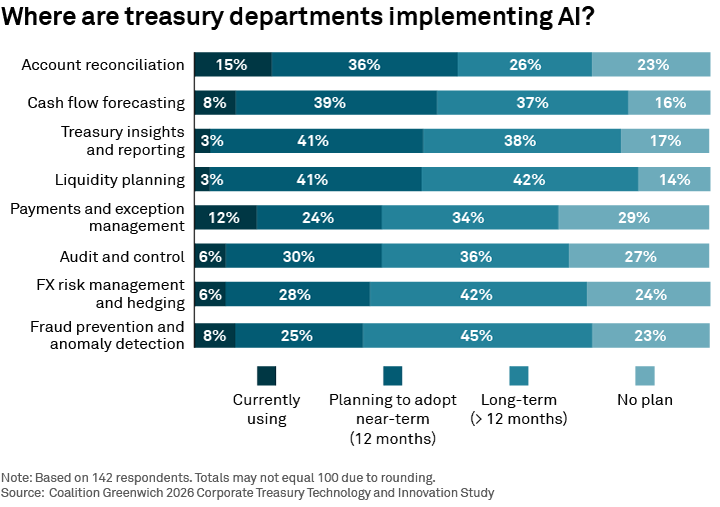

As shown above, more than half of corporate treasury departments are already or expect to be using AI for account reconciliation within the next 12 months, while almost half aim at implementing AI within this short time period for cash-flow forecasting, enhancing treasury insights and reporting, as well as liquidity planning. More than a third are intending to utilize AI by next year for payment and exception management, audit and control, and FX risk management and hedging. Thirty-three percent are already or expect to improving fraud prevention by way of AI tools within the next 12 months. It is equally important to note that over a longer period, more than 75% are planning to implement AI tools in all but two areas that were discussed.

For the most part, study participants seem to be ambivalent about how they acquire these AI solutions. While some companies might build them, and others might buy them directly from technology vendors, many others will utilize AI tools built into the TMS, ERP and other systems they already use and pay for. For example, firms like SAP and Oracle are integrating predictive analytics and other AI applications that harness both the client’s proprietary data and anonymized data from other users.

These providers have a strong incumbent advantage. Their AI applications are already installed and available to treasury staff for experimentation and actual adoption. That’s a good position for treasury departments, who can try out these offerings, figure out if these built-in applications meet their needs, and determine if the benefits of building or buying additional AI tools are worth it.