AI is now being utilized in finance, with applications related to fraud detection, credit scoring and robo-advising. To date, most of these are focused on retail rather than institutional applications, but this is rapidly changing...

We strongly believe the human banker will remain the cornerstone of commercial and corporate banking relationships. Going forward, AI will make bankers more effective in their client interactions by customizing presentations, generating personalized insights and recommendations, and contributing to solutions tailored to individual clients.

AI is now being utilized in finance, with applications related to fraud detection, credit scoring and robo-advising. To date, most of these are focused on retail rather than institutional applications, but this is rapidly changing...

The results of the Greenwich Associates 2016 European Exchange-Traded Funds Study show that institutional investors are turning to ETFs for liquidity, ease of use and fast access to exposures.

Over the past 12 months, relatively large numbers of large companies have changed banks, and a surprising 40% of large companies express a strong willingness to switch banks in the year ahead.

Institutional assets are flowing into exchange-traded funds as U.S. institutions integrate ETFs into essential functions ranging from risk management and liquidity enhancement to...

Institutional investors in 2016 increased budgets to fixed-income trading desks in preparation for shifts in the interest-rate environment, and continued to ramp up IT budgets to keep pace...

Compare salary and bonus versus those of peers by similar tenure and job function.

Compare salary and bonus versus those of peers by similar tenure and job function.

Compare salary and bonus versus those of peers by similar tenure and job function.

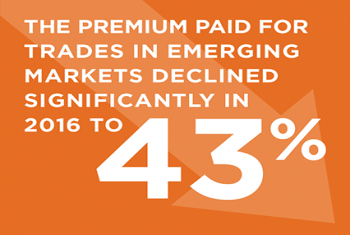

In Q4 of 2016, Greenwich Associates conducted 181 online interviews across North America, Europe and Asia to bring clarity to the commission rates firms pay for equity trades. The result is a truly comprehensive view across 77 MSCI-defined developed...

Exchange-traded funds continue to attract new institutional users and assets in Asia, driven by significant growth among asset managers, institutional funds and insurance companies. The results of the Greenwich Associates 2016 Asian ETF...

Access timely info via personalized dashboard

Receive webinar invitations and set up your preference

Save Coalition Greenwich Research in a personal folder