The unwritten rules of consultant relations: Private markets

In this, our third installment about the unwritten rules of consultant relations, we address a topic that is top of mind for asset managers, asset owners and consultants alike: private markets.

The influx of institutional capital into private assets has triggered fierce competition among managers, including both the private market specialists who have long dominated this space, and large multi-asset managers who have started building out or acquiring private market capabilities.

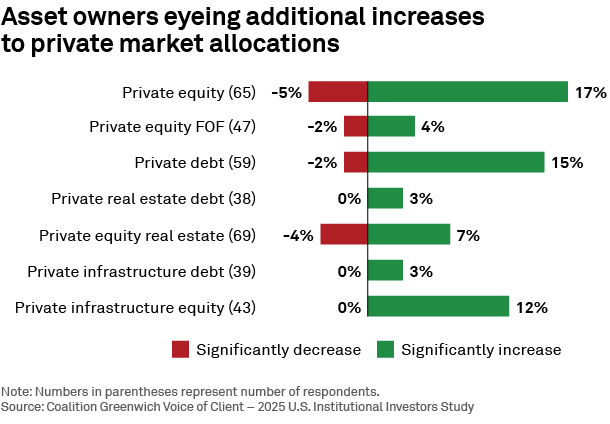

Despite recent headwinds in private credit and a shortage of exits in private equity, institutional investors seem firmly committed to plans to expand allocations to private markets (see graphic below). As they seek the best strategies for taking on private exposures, most institutions will rely on guidance from their investment consultants. However, the nature of that advice—and, in cases, the relationships between institutions and consultants—will differ considerably from the advisory ratings that form the basis of much consultant support in public markets.

For that reason, asset managers competing in private markets need a new playbook for consultant relations.

In addition to extending their traditional role of intermediaries between asset owners and asset managers into private markets, consultants have expanded their capabilities into actually building and implementing private market portfolios. Along with discretionary OCIO businesses, consultants are now building out their own private market funds.

That expanding role in private markets has increasingly put consultants in direct competition with asset managers. Although that can complicate relationships, it does not change the fact that asset managers must maintain strong ties to consultants, who continue to have a powerful influence on asset owners’ selection of managers for their private assets.

How to engage with consultants on private markets

When Crisil Coalition Greenwich interviewed researchers and consultants from the world’s top-tier consulting firms for our most recent industry study, we asked them what asset managers can do to increase their odds of building a strong relationship and receiving ratings on their private market funds. Their answer: Differentiate your firm and fund in the following ways:

- Show that you have a strong and experienced team with a clear and stable organizational structure, proven track record, deep understanding of the market, and well-defined investment philosophy. As one consultant put it: “The stability of the organization and team is probably No. 1, outside of performance and fees.”

- As private markets become more democratized, asset managers can differentiate themselves from the growing crowd by articulating a clear investment strategy and demonstrating a unique value proposition. As one consultant explained: “Having a clearly defined process and being able to articulate areas of differentiation are key. There are so many funds out there. Really acknowledging that and then really being thoughtful about how they articulate their point of differentiation [is what we’re looking for].”

- Demonstrate a strong alignment of interests with investors. Too many asset managers are trying to establish themselves in private markets by pitching products and showcasing returns. Managers have a real opportunity to differentiate themselves by showing their commitment to understanding how their strategies fit into investors’ portfolios and objectives.

- Stand out by being fully transparent in communication, fees and reporting. As one consultant concluded, “Transparency is important and it's becoming more table stakes now. It's important, and we've seen that trending in the right direction already.”

- Consider working with your consultants in areas outside of just diligence (ODD/IDD) and pursuing ratings. Asset managers are building deeper relationships with consultants by implementing aggregated fee agreements, co-investing, and even partnering to launch interval funds.

Close observers might notice one detail in that list that could cause concerns for large multi-asset managers and other organizations that have entered private markets in scale relatively recently. Consultants favor firms with a proven track record and with investment teams that have deep experience in private markets.

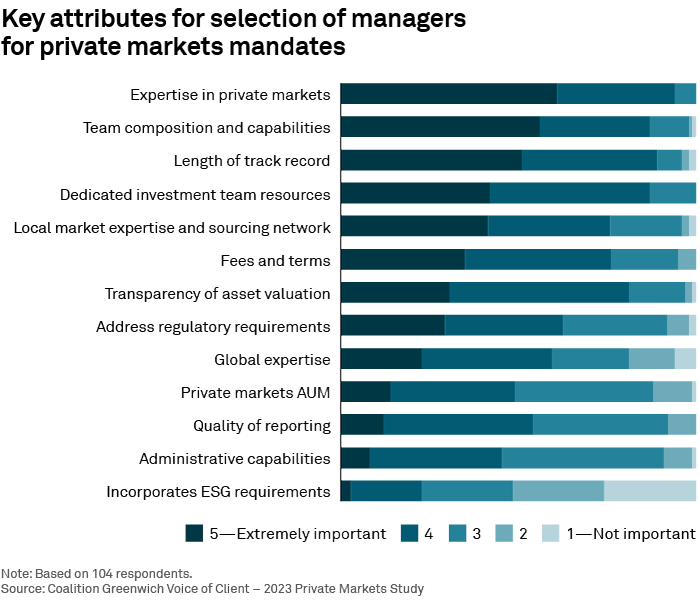

These understandable preferences, which exist among both consultants and asset managers (see following graphic), have created what we call “boutique bias,” or the tendency of consultants to gravitate toward established private market specialists over other competing managers. Although generalist and multi-asset managers have strengths of their own in the form of scale, branding and resources, these results show they will need to be strategic in their approach to private markets.

One way that “generalist” managers have sought to overcome the challenge of boutique bias is by partnering with specialist private market managers. These alliances, like the partnerships between Capital Group and KKR, and Blackstone, Vanguard and Wellington, benefit both sides by providing generalists access to established private offerings and providing specialists with access to massive distribution platforms, often including the wealth channel, insurance and even, potentially, retirement funds.

The consultants participating in our research say that, to this point, these partnerships have yet to trigger any material change to how they interact and do business with those managers. The consultants still have lingering questions about ownership structure and potential conflicts in compensation and incentives arising from differing business models. As one consultant explained, “We have seen a few of them that have worked fairly well. I would say on balance, we probably have a level of skepticism about them.”

The consultants want to make sure that both parties are careful in choosing partners, as these partnerships can be complicated to execute. As one consultant said, “We're trying to understand what the ownership structure looks like, what are the incentives, how do they ultimately pay each other? For now, we're watching and monitoring and figuring out how this will ultimately change things.”

Mixed outlook for private markets

The consultants we interviewed have a mixed outlook for private markets. In private equity, many study participants expect client allocations to remain flat or even decrease due to a recent lack of distributions, underperformance and high valuations. “I don't see the increase in demand being in private equity, given their struggles and returning capital to investors. That's been pretty frustrating,” noted one consultant.

Some consultants think these headwinds will be partially curtailed by increased demand for international private equity as investors seek to diversify their portfolios and tap into growth opportunities outside of the U.S.

The consultants expect to see continued momentum for private credit—at least in institutional portfolios. The consultants say that despite frothy outcomes and volatility that would be expected of any new investment, their institutional clients still see private credit as an emerging asset class with plenty of runway for growth. As one explained, “Private credit, believe it or not, still has some room to grow in terms of clients adjusting their asset allocation to have an allocation there.” On the other hand, the consultants express real skepticism about the prospects for private credit in retail.

Many consultants looking at private markets are focusing on real assets, including infrastructure and real estate, which they believe are getting a boost from improving market conditions and government spending on infrastructure projects.

Across the board, the consultants in the study believe that the boom in private markets will continue as long as public markets remain robust. In particular, they say the strong performance of U.S. public markets has left their clients underweight in private markets.