OTC derivatives volume decreased in 2013.

Featured Blog

How banks can prepare for a future with AI

We strongly believe the human banker will remain the cornerstone of commercial and corporate banking relationships. Going forward, AI will make bankers more effective in their client interactions by customizing presentations, generating personalized insights and recommendations, and contributing to solutions tailored to individual clients.

FX Electronic Trading 2014 - Global Trends and Competitive Analysis

Greenwich Market Trends

February 14, 2014

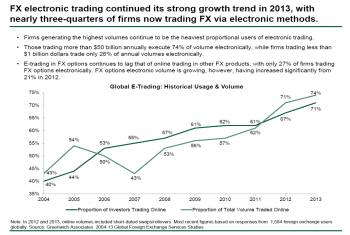

As strong growth continues in FX e-trading, regulatory changes and algorithm usage are driving some users back to single-dealer platforms.

2013 Greenwich Leaders: Asian Equities and Equity Derivatives

Greenwich Awards

The Asian equity market is attracting fierce competition from a large and diverse group of brokers looking to capture a share of the region’s recovering institutional research and trading business.

2013 Greenwich Leaders: Japanese Equities and Equity Derivatives

Greenwich Awards

Mizuho Securities and SMBC Nikko Securities each gained four percentage points or more of vote share in Japanese equity research and advisory services during in 12-month period...

Trading volume increased in 2013.

Although Asian banks have been capturing large corporate clients from European rivals, the latest research from Greenwich Associates shows that HSBC has established itself as the leading bank in the region in terms of both number of relationships...

2014 Greenwich Leaders: European Corporate Banking

Greenwich Awards

BNP Paribas has established itself atop the European corporate banking market by securing relationships with 56% of the largest European companies.

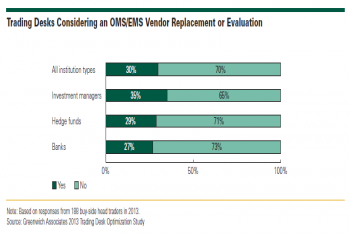

Thirty-nine percent of fixed-income desks reported a year-on-year budget increase and 30% are considering a change in the providers of their order management systems (OMS) or execution management systems (EMS).

HSBC, Citi, Deutsche Bank, and Standard Chartered Bank consolidate share in growing market.

2013 Asian Intermediary Distribution - Product Coverage and Demand - Graphics

Greenwich Market Trends

January 30, 2014

Almost all distributors now distribute emerging market and high yield bonds in addition to money market, domestic bonds and global bonds.

Pages

Access Free Research

Access timely info via personalized dashboard

Receive webinar invitations and set up your preference

Save Coalition Greenwich Research in a personal folder

REGISTER

In The News

-

The Desk: According to Coalition Greenwich, Investment grade E-trading held steady MoM at 49% of...May 19, 2026

-

The Desk: “The market is undeniably in a period of change, as scheduled auctions take share from...May 19, 2026

-

Coalition Greenwich Asset Owner Principles May Support Japanese Institutional Investors' Use of OCIOJ-Money: According to the Crisil Coalition Greenwich Voice of Client – 2025 "Japanese Institutional...May 18, 2026