Say Goodbye to Buy-Side Boom Times

November 18, 2015

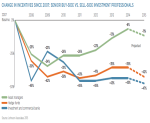

Pay levels in asset management in 2015 are projected to be slightly lower, according to a new report, Say Goodbye to Buy-Side Boom Times, from Greenwich Associates and Johnson Associates.