April 2015

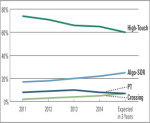

Institutions in Asia are executing a steadily increasing proportion of business on a low-touch basis (algorithms, DMA, crossing, portfolio trades) as opposed to traditional high-touch business executed through a broker sales trader. These same...

Categories:

Equities, Technology, Uncategorized

Free Tags:

Asian Equities, e-trading, technology