Blockchain technology presents a big opportunity for financial services firms.

We strongly believe the human banker will remain the cornerstone of commercial and corporate banking relationships. Going forward, AI will make bankers more effective in their client interactions by customizing presentations, generating personalized insights and recommendations, and contributing to solutions tailored to individual clients.

Blockchain technology presents a big opportunity for financial services firms.

Greenwich Associates provides comprehensive rankings of the most helpful traders and analysts in the United States.

Greenwich Associates provides comprehensive rankings of the most helpful traders and analysts in the United States.

Greenwich Associates provides comprehensive rankings of the most helpful traders and analysts in Canada.

Greenwich Associates provides comprehensive rankings of the most helpful traders and analysts in the United States.

Greenwich Associates provides comprehensive rankings of the most helpful traders and analysts in the United States.

NEPC saw a surge in considerations for new assignments in 2014, though Cambridge and Russell also experienced nice increases as well.

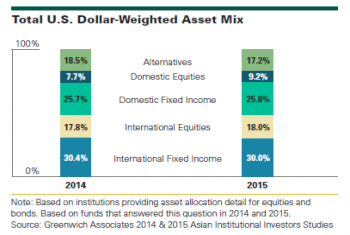

Asset management companies continue to enter the Asian market to fight for a share of the region’s fast-growing pool of institutional investment assets.

While investors' needs and wants are critical to the development of new liquidity pools, dealers must be economically incented to show up to the party.

Total compensation rose for many functions with the remainder holding steady.

Access timely info via personalized dashboard

Receive webinar invitations and set up your preference

Save Coalition Greenwich Research in a personal folder